Life would be far easier for many trustees if investment management was a simple numbers game: a science in which the fastest computer or biggest brain wins. However, in practice, investment is time-consuming and there is much ‘art’ and qualitative analysis required to achieve success.

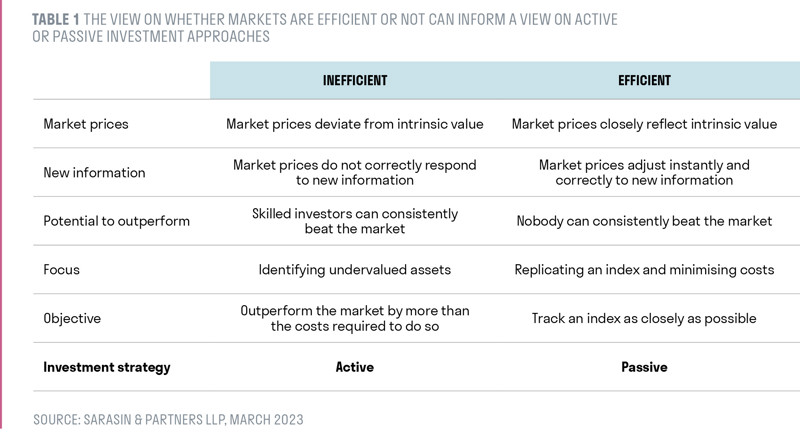

The theory of tracking an index or a range of indices appears to make perfect sense. After all, active managers produce a wide dispersion of returns, making it tough to find a good one. We must also acknowledge that the majority of active managers, after costs, have often lagged indices’ performance.

So why not simplify things: remove manager risk and invest ‘passively’ by owning a fund that simply replicates an index?

Sadly, it isn’t that simple. There are probably as many scenarios in which an actively managed portfolio will deliver a better outcome than a passively managed one, even if the actively managed one underperforms its index-based benchmark. How could this be the case?

Allocating assets is an active decision

If a single asset class is all that is required to meet an investment objective, then buying an index-tracking fund could make sense. However, it is rarely appropriate for a charity to have exposure to just one asset class. Assets are typically blended together to achieve a risk/return profile that ensures your portfolio is aligned with your objectives. Critically, choosing which assets to include in your portfolio and how much is assigned to each, will likely have a significantly greater impact on performance than the return of each asset class, relative to the relevant index return.

Who sets this strategic policy and ensures it is rebalanced on a regular basis? Who ensures it evolves over time, embracing new asset classes or a change in the investment objective? Could it make sense to make tactical shifts between asset classes to reflect medium-term market conditions?

Setting and sticking to an investment strategy is simple, but not easy. All too often portfolios suffer from behavioural mistakes made when market sentiments are at extremes.Keeping a cool head and avoiding these pitfalls require a deep understanding of the underlying asset classes and the ways in which fear and greed can influence decision-making.

All too often portfolios suffer from behavioural mistakes made when market sentiments are at extremes.

The best strategic advice is undeniably valuable and will almost certainly negate any technical underperformance of a given mix of indices. While there are managers and consultants who will blend a range of passive funds together, it is important that any costs associated with this advice and any costs associated with holding and trading these funds are included when performance is reported.

The true worth of any passive or active manager who designs and manages multi-asset portfolios should be measured at the total portfolio level, after the impact of strategy, tactics, stock selection and all costs. Individual elements might not always add value after costs relative to an index – and quite possibly at the portfolio level, against an index of blended indices. However, the overall result is what actually matters, relative to what other managers have achieved.

This, of course, can be measured. The active or passive managers worth considering share their multi-asset portfolios’ performance with independent monitors such as Asset Risk Consultants (ARC) and Morningstar. Any manager that produces top-quartile returns over the long term – regardless of whether the results have been achieved actively or passively – deserves consideration. We should not be lured into thinking we can only measure managers against their ability to match index returns for an individual asset class. The way in which they blend assets together will invariably matter much more.

Picking passive funds is also an active decision

Even if you, your manager, or your adviser chooses to adopt passive coverage of each asset class, there is still risk and the devil is in the detail.

Specifically, there is a huge choice when it comes to picking index trackers and a bewildering array of indices to follow. Unhelpfully, the difference between selecting one index over another to cover a particular asset class can be as significant as appointing the wrong active manager!

For example, just two words account for a 1.2% difference per annum (on average) between two seemingly identical MSCI indices over the past five years.1 The MSCI All Countries World Index (ACWI) and the MSCI World Index (WI) may sound similar, but the former includes emerging market countries, whereas the latter does not. The results between other well-known index providers and the subtle variations they offer often produce even greater differences.

So, the ‘active’ decision that you or your adviser makes about which index you adopt, might well lead to a worse result than selecting an active manager who mildly underperforms a better index that produces a greater return.

These differences can be huge when looking to track other asset classes. For example, the Rogers Commodity Index ETF generated a return of 109% over the 3 years to 31st March 2023, while the L&G All Commodities ETF produced 75%. This is a 34% absolute difference, or 7.5% per annum (on average)2. While both tracking funds did what they said on their respective tins, one set of investors ended up much happier.

Then, there are some asset classes that are ‘un-trackable’ and require significant active decisions to be made. These include infrastructure, renewable energy, private equity, private debt, physical property and hedge funds, to name a few. Including these types of investments in a diversified multi- asset portfolio can help reduce overall portfolio risk and/or enhance returns.

2022 was a good example of a year when virtually every conventional asset class lost investors’ money. An allocation to actively managed ‘alternative’ assets could have reduced the pain.

The ethical consideration

Ethical and stewardship requirements also need to be carefully considered. While it is possible to find or design passive strategies that meet ethical criteria, these funds are often significantly more expensive than their ‘vanilla’ equivalents, as passive managers are not able to exploit economies of scale to the same extent.

Integrating broader ESG criteria is, for all intents and purposes, impossible using passive indices. While passive managers offer a veritable alphabet soup of supposedly ESG-aligned indices, these are reliant on an approach that gives every company an ESG score on a variety of quantitative metrics. There is little correlation across providers on what represents a ‘good’ company. Much like ethical or other customised funds (such as those that hedge currencies), these are again often sold at a much higher fee to the headline index.

Similarly, while passive approaches can theoretically engage with management and exercise their shareholder votes, in practice, the managers of passive funds – with their focus on minimising costs – tend to have disproportionately small teams focused on this element of company ownership. There is also reason to doubt whether company boards truly listen to investors who, by their nature, will never actively buy or sell their shares in response to changes the company does or doesn’t make.

The impact of market distortion

Philosophically, we should also consider the value of independent active managers in their role as price setters in markets. We believe this is probably misunderstood and undervalued. The whole world cannot buy index trackers. Markets are, arguably, already becoming distorted with individual companies being inappropriately valued by their huge influence. There is evidence to suggest that the rise of index tracking has pushed up the values of the largest companies relative to many smaller companies which aren’t included in the indices they track. There is often a disproportionate sale of smaller companies each time an investor goes passive.

A related trend has been the rise of allocations to private equity funds, which often buy these undervalued smaller companies. These small companies can then be combined while in private ownership, before being re-floated as a single entity that is subsequently large enough to be part of a trackable index, at a size that commands a higher valuation.

Herein lies the rub.

One suspects that what has been saved on management fees by adopting passive strategies, has been inadvertently passed across to the private equity industry, where fees can be many multiples higher than passive management. Ultimately, from a cost perspective, the move to index tracking has probably been a zero-sum game for many large investors: markets are remarkably efficient in a multitude of ways, but often not in the ways one expects.

A nuanced decision for investment success

We understand the appeal of low-cost and seemingly low-risk passive investments. However, a more thorough analysis into the difficulties of implementing such an approach successfully makes it a much harder and more nuanced decision.

The best active managers try to help their clients achieve much more than just stock-picking their way to outperforming benchmarks and indices. Ultimately, one pays a multi-asset active manager for their invaluable strategic and tactical asset allocation services, including access to the full range of investment opportunities.

While it would be nice to think that the majority of active managers could outperform indices after costs consistently, this has never been – and is unlikely ever to be – the case. However, this doesn’t mean that the overall results active managers achieve won’t be better, after costs, than many passive alternatives.

[1] Bloomberg, MSCI

[2] Bloomberg

Important information

If you are a private investor, you should not act or rely on this document but should contact your professional adviser.

This document has been approved by Sarasin & Partners LLP of Juxon House, 100 St Paul’s Churchyard, London, EC4M 8BU, a limited liability partnership registered in England & Wales with registered number OC329859 which is authorised and regulated by the Financial Conduct Authority with firm reference number 475111.

It has been prepared solely for information purposes and is not a solicitation, or an offer to buy or sell any security. The information on which the document is based has been obtained from sources that we believe to be reliable, and in good faith, but we have not independently verified such information and no representation or warranty, express or implied, is made as to their accuracy. All expressions of opinion are subject to change without notice.

Please note that the prices of shares and the income from them can fall as well as rise and you may not get back the amount originally invested. This can be as a result of market movements and also of variations in the exchange rates between currencies. Past performance is not a guide to future returns and may not be repeated.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect of any such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct. indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

Neither Sarasin & Partners LLP nor any other member of the Bank J. Safra Sarasin group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of his or her own judgment. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document. If you are a private investor you should not rely on this document but should contact your professional adviser. © 2023 Sarasin & Partners LLP – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin & Partners LLP. Please contact marketing@sarasin.co.uk.