Energy price shocks may boost fossil fuels in the short term, but they tend to accelerate the shift towards cleaner energy and the infrastructure that supports it.

The conflict in Iran, together with the closure of the Strait of Hormuz and attacks on gas facilities in the Middle East, has forced the global economy to adapt to a significant oil and gas supply shock in 2026. The effects are being felt far beyond the Asian and European economies that depend on this shipping route. Even the largely self-sufficient US is not insulated from a global oil price above $100 a barrel.

Leaving aside the profound humanitarian toll, oil and gas price spikes may provide a temporary boost for fossil fuel investors, but caution is still warranted. Over the longer term, the more durable winners may be companies that are helping to drive the transition away from traditional energy sources.

Sarasin has long maintained a nuanced, climate-focused approach to fossil fuels. Where appropriate, however, we also selectively hold some exposure to the sector, via passive funds or in some instances individual companies, such as Shell in our Global Dividend strategy.

We recognise that periods of elevated fossil fuel prices are often seen as a reprieve for the traditional energy sector. Higher oil and gas prices lift revenues, widen margins and, in the short term, tend to support the share prices of energy producers. However, oil and gas companies rarely keep the excessive returns that could be earned from a commodity price spike as governments will often introduce windfall taxes aimed at redistributing these gains. For example, the Energy Profits Levy was introduced in the UK in May 2022.

Yet history suggests that energy crises do not ultimately extend the fossil fuel era. Rather, they tend to accelerate the transition away from it. High fossil fuel prices may support oil and gas companies in the near term, but they ultimately reinforce the economic, political and technological forces driving the global energy transition.

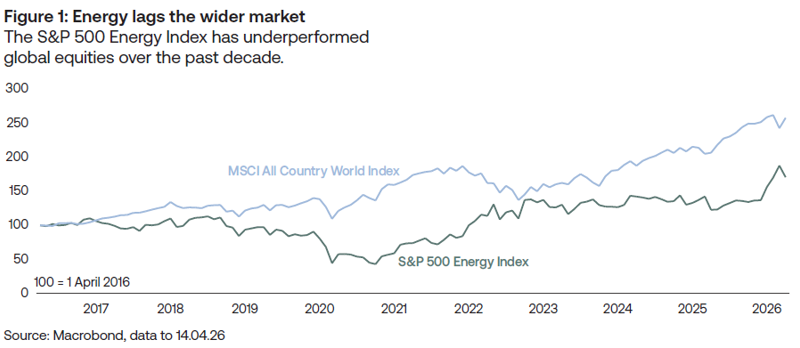

The return data is unambiguous

The performance of global equities over the past decade illustrates this dynamic clearly. Over the ten years to March 2026, the global equity market delivered significantly better returns than from the energy sector alone (as shown in figure 1).

This is not a short-term dislocation; it reflects a structural shift in where value is being created in the global economy. The energy sector’s period of relative outperformance was concentrated in a single episode: the oil price spike of 2022.

As energy markets tightened following Russia’s invasion of Ukraine, energy equities rallied sharply – but this window lasted only around eighteen months. By 2023, much of the relative gain had already unwound. Longer-term returns have instead accrued outside the energy sector, particularly in companies exposed to electrification, grid infrastructure and industrial technology.

Why energy crises undermine fossil demand

Energy crises trigger effects that are structurally negative for long-term fossil fuel demand. This is because households reprioritise spending; driving less, switching to public transport, and reducing discretionary travel. This can accelerate the adoption of electric vehicles. Once consumers switch, they are unlikely to revert.

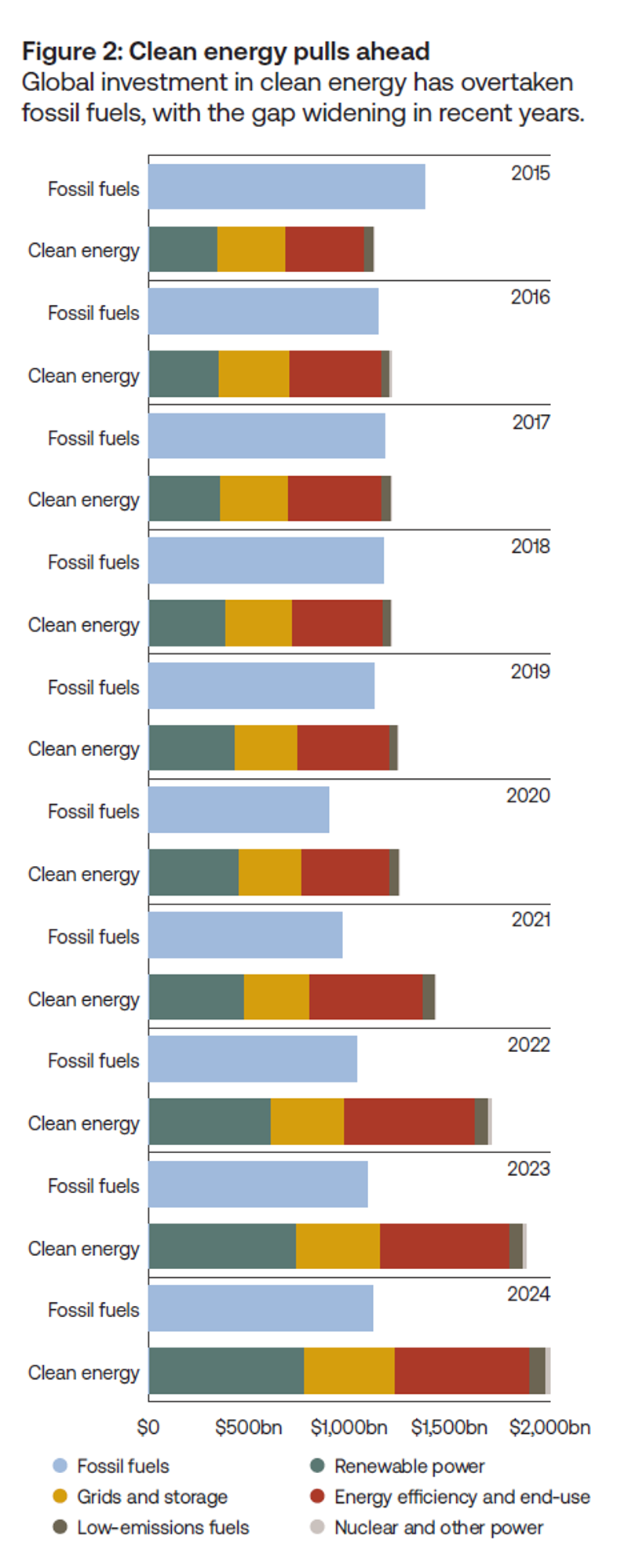

High fossil fuel prices also create a powerful incentive structure for clean energy investment. In 2023, global clean energy investment reached approximately $1.7trn, according to the IEA, the first year in which capital expenditure on clean energy exceeded spending on fossil fuels. In other words, the same price shock that benefits oil producers in the short term also helps finance the infrastructure that will reduce oil demand in the future.

The geopolitical multiplier

The 2022 energy shock amplified a further dimension: geopolitical urgency. Russia’s invasion of Ukraine transformed energy security from a background concern into a central strategic priority, making dependence on imported fossil fuels carry not only an economic cost, but a clear political and security risk. Two policy responses illustrate the scale of the shift. In Europe, the REPowerEU programme committed €210bn by 2027 to eliminate reliance on Russian fossil fuels. In the US, the Inflation Reduction Act allocated $369bn to clean energy manufacturing and deployment. Neither would likely have been politically achievable without the preceding energy price shock.

There is also historical precedent: every major oil price shock since the 1970s has been followed by a surge in policy support for alternative energy technologies. What distinguishes the current cycle is that the economics of these technologies had already improved significantly before the crisis began. Policy is therefore not initiating the transition – it is accelerating one that was already underway.

The cost advantage that does not reverse

A key driver of this transition is the changing cost structure of energy generation, measured by the levelised cost of electricity (LCOE). Over the past decade, renewable generation costs have fallen significantly as deployment has scaled, with solar benefiting from steep learning curves in manufacturing and installation. The key insight is that this process behaves like a ratchet. When costs fall due to technological progress and scale, they rarely return to previous levels. There was a genuine complication between 2021and 2025: supply chain disruption and higher interest rates increased the cost of renewable deployment, with wind and solar LCOE rising. However, the relevant comparison is not with trough levels but with competing forms of generation. Even after these cost increases, utility-scale solar remains broadly competitive with new gas generation and significantly cheaper than gas peaking plants. The transition’s cost advantage has slowed, but it has not reversed.

Return data, capital flows, policy responses and cost curves all point to the same conclusion. Energy crises may temporarily boost fossil fuel profits, but structurally they accelerate the shift towards alternative energy systems. This is not a speculative scenario; it is an observable mechanism evident across multiple datasets over more than a decade.

Importantly, this does not mean fossil fuel companies will cease to generate cash flows. The more significant question for investors is not whether the energy transition continues, but where value will accrue within it. Historically, the majority of returns have not come from the technologies that directly replace fossil fuels, but from the infrastructure and industrial systems that enable the transition. Electrification requires substantial investment in power networks, grid management, industrial equipment and raw materials.

Examples from our global buy list include power infrastructure providers such as Schneider Electric, grid and electrification specialists such as Quanta Services, and producers of critical transition metals such as Freeport-McMoRan and BHP. These businesses sit upstream in the supply chain and benefit from the broad expansion of electrified infrastructure, regardless of the precise mix of generation technologies.

A transition accelerated, not delayed

The global energy system is undergoing one of the most significant structural shifts in modern economic history. Commodity markets will remain volatile, geopolitical tensions are likely to persist, and fossil fuels will continue to play a role in the global energy mix for many years. Yet the direction of travel is increasingly clear. High fossil fuel prices compress the payback period for alternative technologies, often to fewer than five years in many markets.

Renewable technologies continue to benefit from powerful learning curves. Record levels of capital investment are reinforcing these dynamics each year. Paradoxically, the very events that appear to strengthen the fossil fuel sector in the short term often accelerate the forces that weaken it over the longer term. For investors looking beyond the immediate cycle, the opportunities created by the energy transition are likely to reside less in the fuels being displaced and more in the systems and infrastructure that enable the new energy economy to function.

Important information

This document is intended for retail investors and/or private clients. You should not act or rely on this document but should contact your professional adviser.

This document has been issued by Sarasin & Partners LLP of 50 George Street, London W1U 7DY, a limited liability partnership registered in England and Wales with registered number OC329859, and which is authorised and regulated by the Financial Conduct Authority with firm reference number 475111.

This document has been prepared for marketing and information purposes only and is not a solicitation, or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice.

This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2026 Sarasin & Partners LLP – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin & Partners LLP. Please contact marketing@sarasin.co.uk.