The performance of global equities in the second quarter of the year was a textbook example of markets climbing a wall of worry. By the beginning of July, the MSCI World index sat above its level on the eve of President Trump’s “Liberation Day” on 2 April.[1] This is despite the highest US tariffs in nearly a century, three simultaneous Middle Eastern conflicts, and direct US strikes on Iran’s nuclear facilities. In more ‘normal’ times, any one of these events might have triggered a surge in oil prices, a stronger dollar, and a sharp equity sell-off. This time, we saw the reverse.

Unexpected outcomes have emerged in Europe too. Intensifying conflict in Ukraine – combined with renewed American pressure to “share the burden” – has prompted European governments to commit to significantly higher defence spending.[2] Ordinarily, such moves would unsettle equity markets and support the dollar. In fact, the euro strengthened while European equities rallied, led by banks, industrials, and defence stocks.

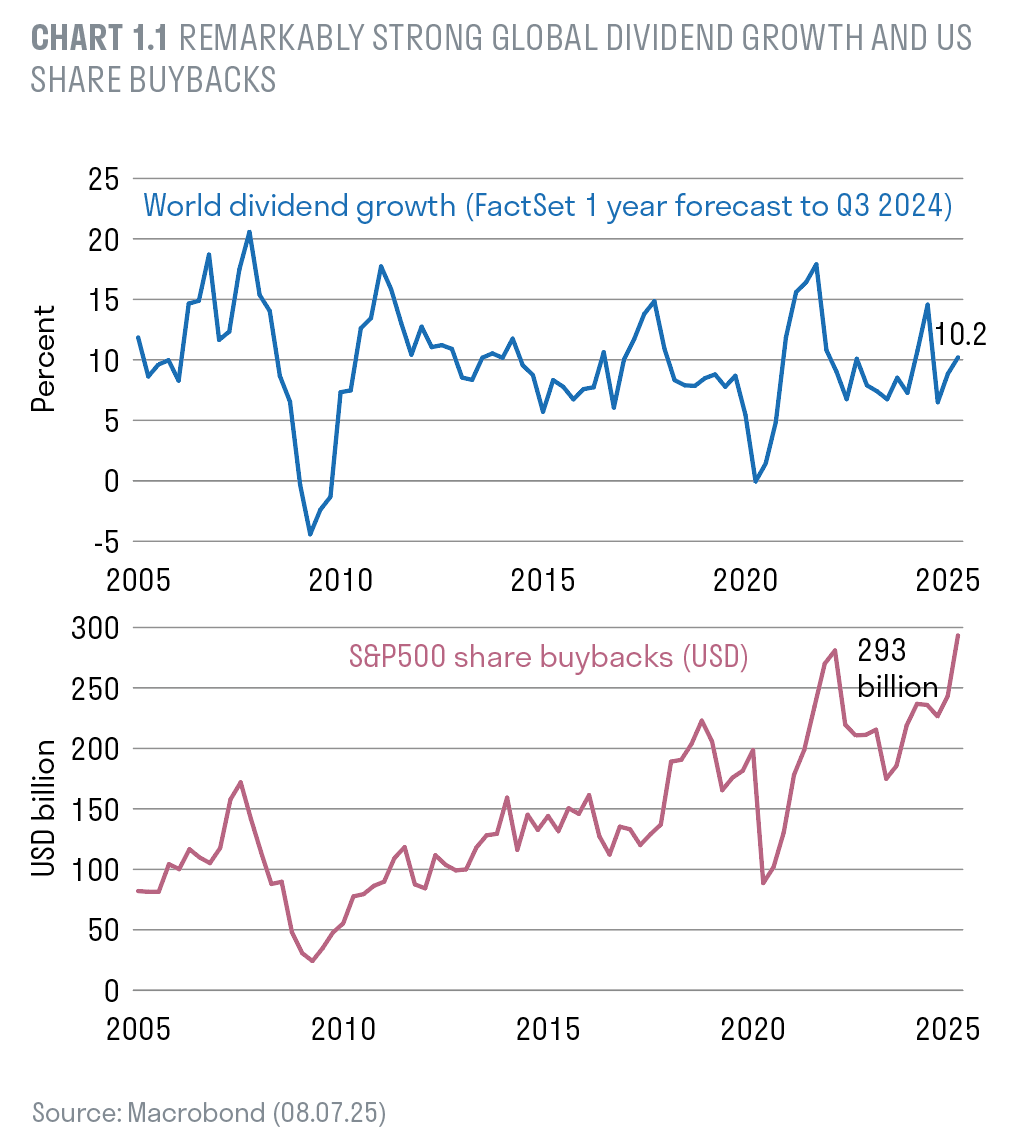

A similarly counterintuitive pattern can be seen in Washington, where President Trump’s tariff programme continues to advance. Current projections suggest the average US tariff rate may settle around 15% or higher – a level not seen since the days of the Smoot-Hawley Act.[3] Yet, rather than focusing on short-term inflationary risks, investors have largely looked through the noise and revised global earnings forecasts upward. Global dividends are projected to rise more than 10% this year, while US share buybacks hit record levels last quarter (Chart 1).

Why are markets rallying?

Why, against one of the most turbulent geopolitical backdrops in a generation, are markets rallying?

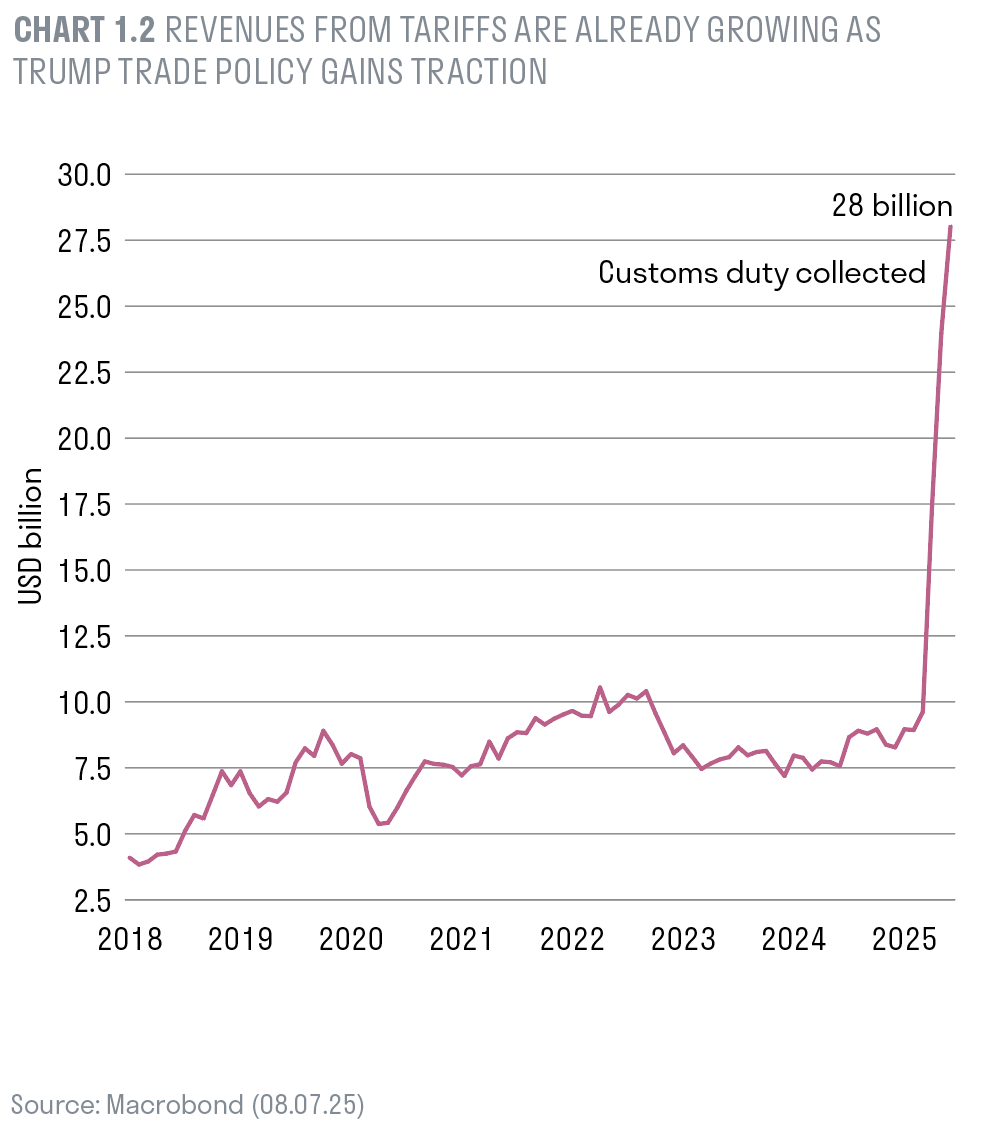

Part of the answer lies in shifting perceptions of the Trump White House. Beneath the rhetoric, investors are starting to identify elements of economic logic that appear broadly market-friendly. The US trade deficit, now approaching 5% of GDP, is plainly unsustainable.[4] A moderate tariff regime – particularly one aimed at dismantling informal trade barriers – may yet succeed where other strategies have failed (as you can see in Chart 2, tariff revenues are already climbing). Meanwhile, the inflationary effects of tariffs have yet to show up meaningfully in US data. The Fed’s preferred measure, the Core PCE Deflator, remained steady at 2.7% for May.[5] On the geopolitical front, it may also be argued that US strikes on Iran’s nuclear sites have reduced rather than heightened global risks. The targeted action appears to have delayed uranium enrichment efforts long opposed by Washington, its allies, and Gulf partners. Iranian retaliation was limited – possibly even pre-signalled – and the broader economic fallout has been negligible. At the time of writing, oil prices (WTI) are more than 20% lower than a year ago,[6] while the dollar, which typically strengthens in periods of stress, has fallen by more than 10% this year.[7]

Outside the economic sphere, the administration’s immigration policies have also had a measurable impact. Whatever the longer-term debate, illegal border crossings have fallen dramatically – indeed, to near-zero – on both the southern and northern US borders.[8] Compared to the ongoing immigration challenges in Europe and the UK, the White House appears to have delivered its objectives with surprising effectiveness.

Thematic high-quality companies for the long term

Against this backdrop, we have gradually added risk back to portfolios. We lifted our equity exposure back to neutral in late June as earnings forecasts continued to rise. We maintained our underweight to fixed income, particularly in corporate bonds, where spreads remain tight by historical standards. We have also kept our core positions in physical gold, anticipating ongoing central bank buying from China and other BRICs (Brazil, Russia, India, China) members, seeking more ‘security’ for their reserve holdings.

Our main challenge has been a quality bias in our stock selection where we have favoured companies with high returns on equity, low financial leverage, and stable earnings.

While this protective strategy limited drawdowns in the post-tariff sell-off, it also meant that we were slower to capture the strong market recovery of the last two months. While our AI-related technology holdings performed well, our quality tilt left us looking too defensive versus broader market indices.

Looking ahead, however, we expect our high-quality companies to outperform over the full business cycle. Tariffs will not be painless: margins will be squeezed, and US consumers will eventually face higher import costs. Asian economies with large manufacturing surpluses are likely to divert output to Europe, pushing down prices and placing further pressure on profitability. China’s producer prices have been falling for three years meaning deflation in goods price is now entrenched.[9] To protect margins, Western firms will need robust balance sheets and defensible market positions.

Our Security theme

Many of these “quality winners” feature in Sarasin's new Security theme. This theme focuses on industries where competition is structurally constrained. Strategic supply chains –spanning metals, mining, semiconductors, and defence (BAE Systems has been added to our global equity

buy list) – are fast becoming national priorities. Over time, food security (John Deere), energy, and communications infrastructure (recent attacks on undersea cables have triggered protective measures) will also fall under this umbrella. Cybersecurity, too, is vital –Fortinet is widely held, and is a global leader in network IT defence. You can read more about this sector following our analysts’ visit to Silicon Valley on page 20.

In Europe, deeper domestic capital markets are needed to support more autonomous growth. Bank consolidation is likely to accelerate, and national champions, such as ING, will be favoured. More broadly, as government spending rises, yield curves should steepen – supporting bank earnings

globally, benefiting firms like J.P. Morgan.

Climate resilience also fits within our Security framework. As temperatures rise and extreme weather becomes more frequent, the economic cost of inaction is growing. Despite the current US administration’s scepticism, investments in climate-friendly technologies – at the right valuations – form an important part of our portfolio.

Debt and duration: another case for quality

There is another reason to focus on quality: government debt. A decade of low real interest rates has made heavy borrowing all too tempting, particularly in the US, UK and France. Much of this debt has funded social transfers rather than productive infrastructure. In the US, successive administrations have failed to reverse the trend of widening deficits and rising interest costs. Moody’s downgraded America’s credit rating in May,[10] and the President’s “Big Beautiful Bill” is projected to add $3–3.4trn to the national debt over the next decade.[11] In the UK, high debt levels have constrained Chancellor Rachel Reeves between a left-leaning Labour majority that resists spending cuts and a bond market demanding fiscal discipline. On the broadest measure – tax revenue as a share of GDP – the UK has not seen a peacetime burden this high since the late 1940s. The OBR now forecasts it will climb to a new high of 38% by 2027–28.[12]

Enter the bond vigilantes

Rising debt levels imply higher real rates, steeper curves, and the growing influence of bond market “vigilantes”. More indebted economies may struggle to respond to future shocks, as seen during the global financial crisis and the Covid pandemic.

In the US, a bond market shock is becoming increasingly plausible – in response we have cut positions in dollar mandates and introduced some inflation-linked debt, where appropriate. At the time of writing, French 10-year yields were higher than those in Portugal or Spain, and nearing

Italian levels.

This backdrop justifies our continued caution around bonds (indeed my colleague Michael Jervis dives into some of the detail behind our analysis on page 15), and also reinforces the case for gold. In our target return strategies, we also see value in equity protection, particularly while volatility remains low.

Summary

As the Trump administration’s policies evolve – often erratically and noisily – it is becoming clear that some are proving market friendly. His focus is on deregulation, lower energy prices and corporate tax cuts, even if this builds pressure on government Budget deficits further out. His foreign policy, though unconventional, often seeks to reduce rather than amplify risk. Add to this a strong corporate earnings outlook, accelerating dividends, and record share buybacks, and the case for equities remains compelling.

Still, equity valuations are rich, and many of the early movers – particularly in Europe and Asia – have already rallied hard. In this context, we believe portfolios should be built around global security themes, anchored in quality holdings, and structured to withstand any future storm in sovereign debt markets.

[1] https://www.msci.com/www/fact-sheet/msci-world-index/05830501

[2] https://www.consilium.europa.eu/en/press/pressreleases/2025/07/08/council-activates-flexibility-in-eu-fiscal-rulesfor-15-member-states-to-increase-defence-spending/

[3] https://www.cnbc.com/2025/04/03/us-tariff-rates-under-trumpwill-be-higher-than-the-smoot-hawley-levels-from-greatdepression-era.html

[4] https://www.bea.gov/data/intl-trade-investment/internationaltrade-goods-and-services

[5] https://www.bea.gov/data/personal-consumption-expendituresprice-index-excluding-food-and-energy

[6] https://markets.businessinsider.com/commodities/oil-price?type=wti

[7] https://www.marketwatch.com/investing/index/dxy

[8] https://www.cbp.gov/newsroom/national-media-release/cbpreleases-may-2025-monthly-update

[9]https://www.cnbc.com/2025/07/09/china-producer-prices-falljune-biggest-drop-nearly-two-years-deepening-price-warcpi-ppi-nbs.html

[10] https://www.moodys.com/web/en/us/about-us/usrating.html

[11] https://www.reuters.com/legal/government/view-us-houseapproves-trumps-mega-budget-bill-2025-07-03/

[12] https://obr.uk/efo/economic-and-fiscal-outlook-march-2025/

Important information

This document is intended for retail investors and/or private clients. You should not act or rely on this document but should contact your professional adviser.

This document has been issued by Sarasin & Partners LLP of Juxon House, 100 St Paul’s Churchyard, London, EC4M 8BU, a limited liability partnership registered in England and Wales with registered number OC329859, and which is authorised and regulated by the Financial Conduct Authority with firm reference number 475111.

This document has been prepared for marketing and information purposes only and is not a solicitation, or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice.

This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2025 Sarasin & Partners LLP – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin & Partners LLP. Please contact [email protected].