Key points

Governments are funding defence, public services, and AI investment simultaneously, placing unprecedented demands on capital.

In a regime of Global fragmentation, inflation, bond yields and market volatility are likely to stay higher than investors have become used to.

This regime strengthens the case for equities, tangible assets, and active management, while reducing the appeal of fixed income and the US dollar.

For decades, the classic economic trade-off between defence spending (guns) and social investment (butter) felt like a tidy thought experiment for economics undergraduates, not a live political crisis. The trade-off itself is nothing new. It dates back at least to economist Paul Samuelson’s influential work (first published in 1948), which used guns and butter to illustrate opportunity cost: any resources a state devotes to defence are resources unavailable for everything else.

Fast forward to today. Across the Western world, governments are being confronted with competing demands: pour money into missiles, warships, and military readiness in a fragmenting world, or protect the hospitals, housing programmes, and welfare nets that citizens were promised and have come to depend upon. With defence budgets under intense pressure from a resurgent Russia, an assertive China, a US increasingly reluctant to underwrite European security, and a NATO target of 3.5% GDP by 2035 (of which at least 3.5% is for core military expenditure), defence is surely a must? Cuts to welfare when ageing populations are driving up the structural costs of healthcare and pensions year on year? Unpopular to say the least.

Tricky choices, then. Or are they? Many governments are refusing to choose at all – putting public finance under pressure. Let’s take a look at how we interpret this at Sarasin through the two lenses that matter most to us – market regimes and investment themes – and what it all means for our asset allocation.

Public finances under pressure

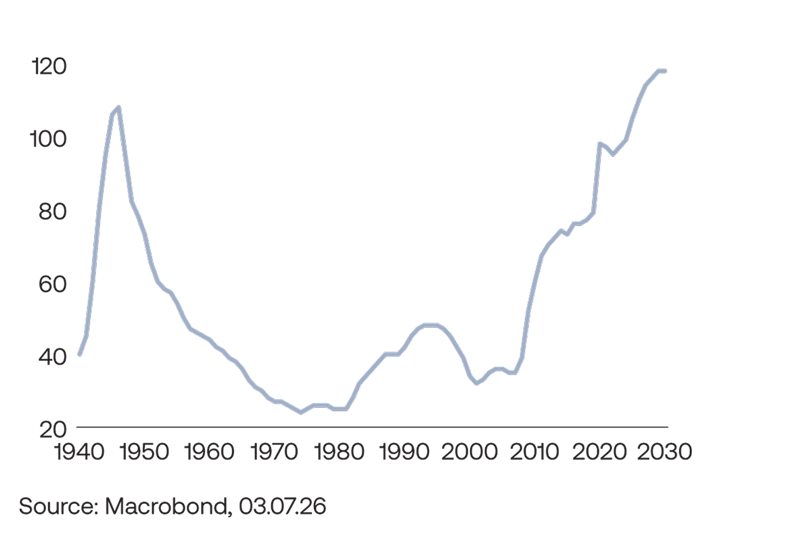

Public finances in most major democracies never fully recovered from the double shock of the 2008 financial crisis and the Covid-19 pandemic. Debt loads are historically high (figure 1 shows an example from the US), and borrowing costs have risen sharply after a decade of near-zero interest rates, adding to the interest cost. This trend is set to rise, not only in the US, which is the relative leader in defence spending (figure 2), but in other areas too, where significant shortfalls have accrued after years of underspending. In short, the so-called peace dividend has gone.

Figure 1: Borrowing to bridge the gap

US government debt has risen sharply over the past two decades.

Implications for economics

What happens to economies when governments choose both guns and butter, and borrow to pay for them? First and foremost, more inflation. Persistent fiscal stimulus adds demand to economies that – in a fragmenting world of tariffs, re-shoring and less reliable supply chains – are less able to meet it cheaply. We therefore expect inflation to be both higher and more volatile than we have become used to. Put simply, we believe 2% is likely to prove the floor, not the average in most developed economies.

“What happens to economies when governments choose both guns and butter, and borrow to pay for them? First and foremost, more inflation.”

Second, stronger nominal growth. Government spending has to land somewhere, and it shows up in nominal GDP – which has been strikingly strong in recent years. This provides a particularly favourable backdrop for companies to grow their sales – and therefore profits.

But there’s more. Guns and butter are not the only claims on capital today; a significant third lever exists in the form of semiconductors. The vast capital expenditure flowing into AI infrastructure is leading to huge amounts of spending, with semiconductors at the epicentre (see Investment focus on pages 22–29). Time will tell whether these investments will be profitable over the long run. But for now we can say that, unlike some investment booms of the past, spending is accompanied by rapidly growing revenues, albeit from a very low base.

How do we summarise all this?

At Sarasin, we analyse these trends as part of our market regime work, which considers the underlying foundations on which an investment environment is built. Typically an investment regime lasts between 10 and 20 years. We believe this one, Global fragmentation, has been in place since 2021. The post-pandemic global economy is shifting decisively away from an open, co-operative framework towards a more fragmented system dominated by power politics and heightened geopolitical insecurity.

Governments spending freely on guns and butter alike (with chips laying claim to capital too) sits squarely within this regime. Its key assumptions are that inflation, bond yields and nominal growth will all be higher than we are used to, that economic and market volatility will pick up, that bonds will be a less reliable diversifier of equities, and that fiat currencies will continue to lose value as inflation runs hot.

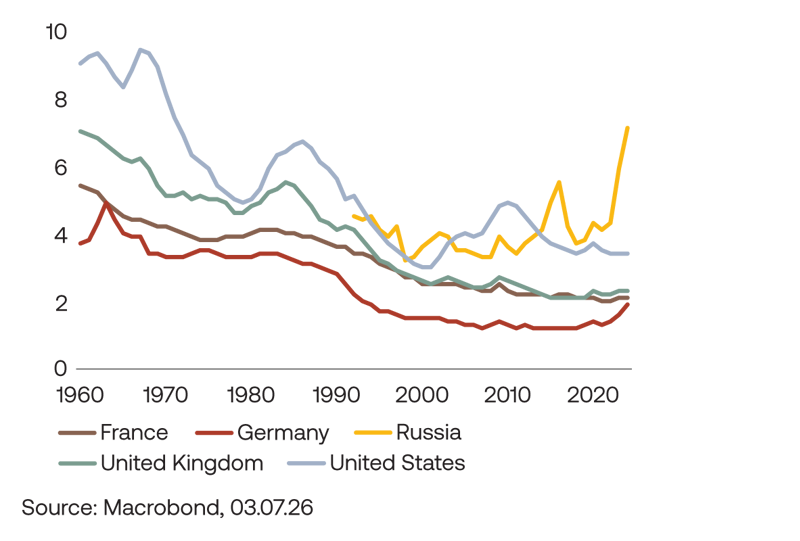

Figure 2: Rearming the West

Military spending is rising in major economies, with Russia increasing expenditure the fastest.

What does this mean for asset allocation?

This regime has clear implications for asset allocation, as reflected in Sarasin portfolios. In particular, high inflation and nominal growth support corporate revenues and profits, and so argue for an overweight to equities, most of the time. There will be exceptions, and fundamentals will always play their part, but that is our natural starting point in this regime.

High inflation, elevated term premia, and reduced diversification benefits also argue for an underweight to fixed income, most of the time. Short-dated inflation-linked bonds are held in some portfolios given the heightened inflationary outlook.

In place of bonds, alternatives are playing a growing role. Ongoing debasement of fiat currencies and rising geopolitical risk point to a strategic allocation to gold, something Sarasin has held for some time. Central banks appear to agree: many have been steadily adding to their gold reserves even as their appetite for US Treasuries wanes. Finally, as the world gradually becomes more multipolar, the dollar’s exorbitant privilege should gradually erode, arguing for a medium-term underweight to the greenback. One way we express this view is through emerging market local-currency debt – more a currency position than a bond one – which we expect to benefit as the dollar weakens.

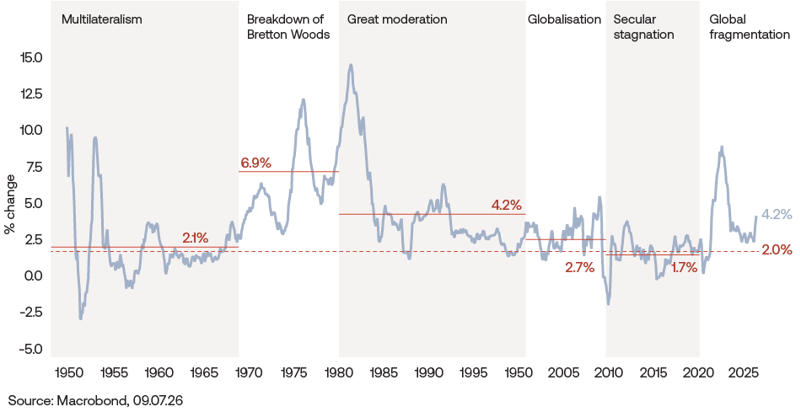

Figure 3: Inflation changes with the regime

Average inflation varies sharply across the six post-war market regimes, including in the current regime of Global fragmentation. This suggests 2% is more likely to be the floor than the long-term norm.

What does this mean for security selection?

As an active equity investor, we see how pressures on public spending can impact different sectors and this informs how we invest given our thematic approach. For example, in 2025, we introduced the new core theme, Security, reflecting not just the ‘guns’ element of defence, but also the impacts of the current regime on global trade, supply chains and food or energy security. Within Security, we invest across cyber security and defence contractors, resource security – from miners to agricultural equipment makers – and ‘protected markets’ such as domestic banks. That all sits alongside our other five longstanding themes.

There are profound shifts in the investment landscape to navigate. We believe our portfolios are well aligned to deal with the challenges this regime presents. However, more than ever, an active approach to strategy setting, asset allocation and security selection is key.

Important information

This document is intended for retail investors and/or private clients. You should not act or rely on any information contained in this document without seeking advice from a professional adviser.

This is a marketing communication. Issued by Sarasin & Partners LLP, 50 George Street, London, W1U 7DY. Registered in England and Wales, No. OC329859. Authorised and regulated by the Financial Conduct Authority (FRN: 475111). Website: www.sarasinandpartners.com. Tel: +44 (0)207038 7000. Telephone calls may be recorded or monitored in accordance with applicable laws.

This document has been produced for marketing and informational purposes only. It is not a solicitation or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice. This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

Capital at risk. The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2026 Sarasin & Partners LLP. All rights reserved. This document is subject to copyright and can only be reproduced or distributed with permission from Sarasin & Partners LLP. Any unauthorised use is strictly prohibited.