View from the desk of the Chief Market Strategist

The second quarter of 2026 was one of the strongest for global equities since the post-Covid recovery almost six years ago. Led by Japan's NIKKEI index, all the major equity markets advanced strongly, supported by continued upward revisions to corporate earnings expectations for the year ahead. The standout performers were chipmakers and memory stocks, which generated extraordinary returns in South Korea, Taiwan and across the US semiconductor sector.

The resurgence in global equities certainly defied the sceptics, coming in the face of war, an oil supply shock and economic forecasts warning of slowing growth. Yet, once again, many of these headwinds have proved transitory. The US-Iran ceasefire, very fragile though it remains, has already triggered a 20% fall in oil prices over the past month despite the recent hostilities by both parties. This can still help cap global inflation and allow central banks to remain on hold, or tighten policy more gradually, through the rest of 2026.

Our multi-asset portfolios remained overweight equities throughout the quarter and have benefited strongly from the market rally. We have also generated positive, albeit more modest, returns from UK government bonds and our alternatives portfolio, where absolute return funds and infrastructure have been the strongest contributors. These gains have more than offset the drag from weaker gold prices, where we have been steadily reducing positions following the precious metal’s record-breaking rally in 2025.

Everyone needs capital

The dominant market theme this year has been the extraordinary surge in AI-related capital investment. Current estimates suggest that the four leading hyperscalers (major cloud providers) will spend around US$725bn on data-centrerelated expansion in 2026 – a figure that is only 20% smaller than the entire US defence budget in 2025. Following visits by our analyst team to several of the AI leaders last quarter, we believe this investment cycle is not only likely to continue but also to broaden. Demand extends well beyond computing power to memory, storage, networking, optics, power infrastructure and cooling. As AI investment ripples across the wider economy, so too will demand for electricity, batteries and industrial metals, particularly copper.

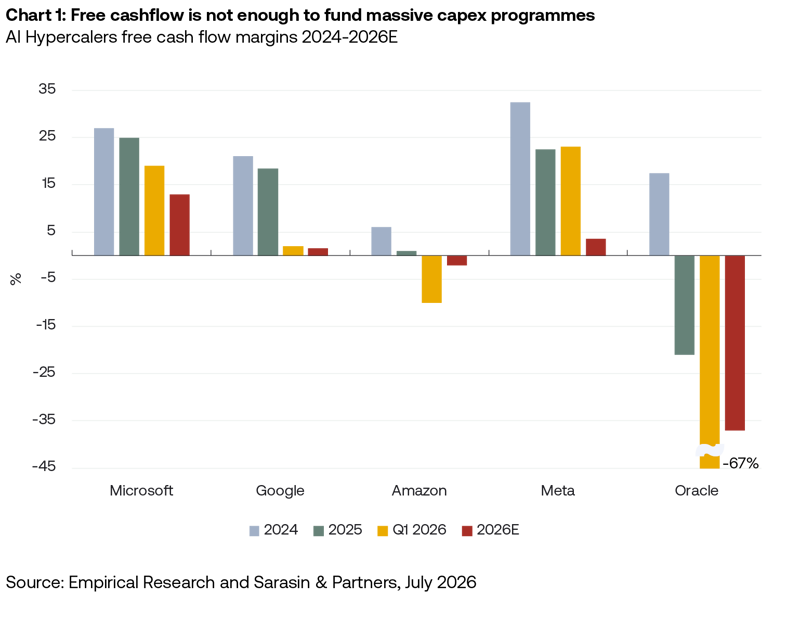

Against this backdrop, the challenge for investors may come less from earnings or valuations than from the unprecedented demand for capital needed to finance the global AI build-out. Until recently, much of this investment was funded from the exceptional cash flows generated by the hyperscalers’ core businesses. That is no longer enough (see chart 1). Capital spending is now outstripping even these formidable resources, forcing companies to tap both equity and debt markets. In June, Alphabet alone raised US$85bn through a follow-on share offering, arguably the largest secondary issuance ever undertaken by a listed company. We also saw the new listing of SpaceX, in what was the largest public offering on record, with Anthropic and OpenAI expected to list in 2026 or early 2027.

Debt markets are also helping to finance the AI build-out, often with remarkably long maturities. SpaceX and Nvidia have both issued 20- and 30-year bonds. Alphabet went further still in February, issuing a tranche of 100-year sterling bonds as part of a broader financing programme. Investors have been attracted by their strong credit ratings – Microsoft debt has a AAA credit rating – Amazon, Meta and Alphabet are all rated AA- (higher than the French sovereign rating).Yet there is an irony here. AI-linked companies are issuing long-dated debt in what is one of the fastest-changing industries in history. Predicting which firms will dominate in 10 years’ time is difficult enough; doing so over the next 100 years is another matter entirely. For that reason, alongside today’s very narrow credit spreads we remain broadly underweight corporate bonds.

Government investment programmes are also competing for capital

The surge in private-sector fundraising comes on top of an equally daunting financing challenge for governments. Across the developed world, states are being forced to spend more on defence, climate resilience and ageing populations. They must also strengthen supply chains, improve national security and, in many cases, rebuild depleted strategic oil reserves.

Two recent developments illustrate how national strategic priorities are driving demand for capital. First, the US administration’s decision in June to restrict access temporarily by certain non-US users to some of the most advanced AI models (Anthropic’s Fable 5 and Mythos 5) reinforces the case for countries to develop at least part of their AI capability domestically. That, in turn, implies another wave of investment in AI infrastructure. Second, the wars in Ukraine and Iran have intensified the drive to build comprehensive missile-defence systems across much of the developed world. At the end of June, the UK government announced a £790m four-year programme to strengthen protection against missile, drone and airattacks. Similar spending plans are emerging elsewhere – Security is one of our key themes at Sarasin.

How will central banks react to an investment boom?

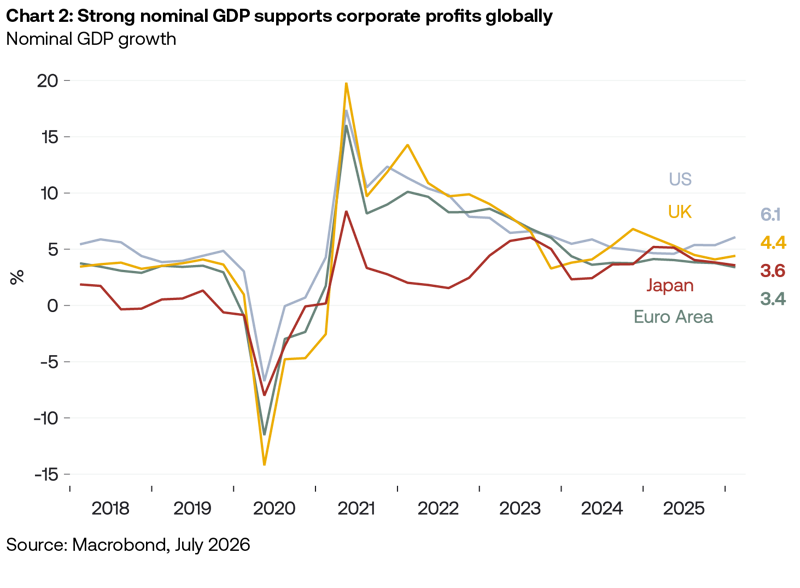

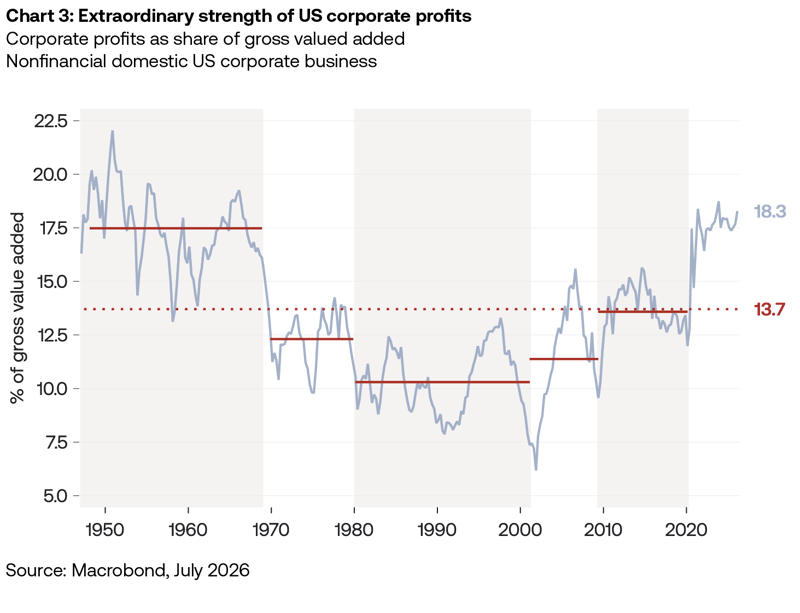

For the first time in several years, the greater risk may be that the US economy overheats rather than slows. Nominal GDP growth is running above 6% (charts 2 and 3), while both the manufacturing and services ISM surveys remain firmly in expansionary territory. Meanwhile, tariff revenues are well below the levels envisaged in President Trump’s original “Liberation Day” proposals, as much of the burden has been absorbed by America’s trading partners with only a modest impact on economic activity.

The challenge for the new Federal Reserve Chair, Kevin Warsh, is that financial markets may be underestimating the inflationary consequences of the sustained global investment boom we have described. Monetary and fiscal policy remain broadly accommodative, while asset prices continue to rise and the resulting wealth effect is supporting consumer demand. The sharp fall in oil prices has provided welcome relief but may not be enough to offset these broader inflationary pressures.Our central expectation remains that US interest rates will stay close to current levels through to mid-2027. However, if growth continues to surprise on the upside, further rate increases cannot be ruled out.

Britain's fiscal credibility will be tested

Britain enters this period of global competition for capital in a relatively fragile position. Barring the wholly unexpected, Andy Burnham will soon become Britain’s seventh prime minister in a decade, inheriting difficult choices over spending, taxation and borrowing. Although energy prices have fallen and gilt yields have declined in recent weeks, the UK continues to face the highest government borrowing costs in the G7 by a considerable margin.

In a world where capital is becoming scarcer and more selective, fiscal credibility will matter as much as monetary policy. Investors will want evidence that the new government is prepared to confront the long-term pressures of welfare spending, pensions and an ageing population rather than just postpone difficult decisions. Clear priorities, credible fiscal discipline and honest communication would go a long way towards reassuring bond markets. Failure to deliver them would leave the UK particularly exposed.

That balance of risks underpins our neutral position in UK government bonds. Current yields are attractive, but they also reflect the fiscal challenges. We continue to expect the Bank of England to largely look through the inflation spike from higher energy prices as far as possible, before a gradual easing cycle begins from the middle of 2027.

So, what does this scramble for capital mean for portfolios in the year ahead?

Elevated spending by both governments and the private sector should keep the US economy running hot into 2027. Europe and Asia, meanwhile, will benefit from sharply lower oil prices as the Strait of Hormuz gradually reopens. Robust US nominal GDP growth should help deliver the near-30% rise in global corporate earnings expected by analysts over the next 12 months, supporting our continued overweight position in global equities.

Government deficits are likely to remain large despite strong economic growth, with little political appetite for fiscal restraint. Higher fiscal and inflation risks should keep term premia elevated and bond yields higher for longer. We therefore remain underweight fixed income.

Countries facing political uncertainty will remain vulnerable to bond-market vigilantes, as the UK has already discovered. In a world where capital has abundant alternatives, investors will demand credible fiscal discipline and clear spending priorities. We expect a weaker dollar over the longer term while expecting emerging market currencies to broadly appreciate.

More fragmented and less efficient global supply chains are likely to leave inflation both higher and more volatile. National security concerns will encourage countries to localise critical infrastructure and intellectual property rather than depend on geopolitical rivals. This strengthens the longer-term case for tangible assets including energy, food, industrial metals, rare earths and potentially batteries.

The diffusion of AI should accelerate, lifting productivity, sustaining strong nominal growth and generating robust profits across an expanding AIsupp ly chain. As businesses adopt AI more widely, productivity gains should increasingly extend beyond the technology sector, creating opportunities across the broader economy.

Higher fiscal deficits and greater geopolitical uncertainty should reinforce demand for gold and other scarce real assets as stores of value.

The result of all this is an unusually intense competition for capital. Governments and companies alike are racing to finance vast investment programmes spanning AI infrastructure, defence, energy security and climate resilience. The consequence will be a global scramble for savings – one that reshapes market leadership, raises the cost of capital and emerges as one of the defining investment themes of the decade.

Important information

This document is intended for retail investors and/or private clients. You should not act or rely on any information contained in this document without seeking advice from a professional adviser.

This is a marketing communication. Issued by Sarasin & Partners LLP, 50 George Street, London, W1U 7DY. Registered in England and Wales, No. OC329859. Authorised and regulated by the Financial Conduct Authority (FRN: 475111). Website: www.sarasinandpartners.com. Tel: +44 (0)207038 7000. Telephone calls may be recorded or monitored in accordance with applicable laws.

This document has been produced for marketing and informational purposes only. It is not a solicitation or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice. This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

Capital at risk. The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2026 Sarasin & Partners LLP. All rights reserved. This document is subject to copyright and can only be reproduced or distributed with permission from Sarasin & Partners LLP. Any unauthorised use is strictly prohibited.