Geopolitics, climate pressures, and rising energy costs are reshaping the global food system. As fertiliser prices rise and supply chains become more fragile, food inflation is increasingly reflecting a broader shift towards a more fragmented and volatile world.

For many years, food prices were relatively stable across most developed economies. Global supply chains became more efficient, energy was abundant, and agricultural productivity continued to improve. Consumers began to spend a smaller share of their household wallet on food than other goods.

That backdrop is beginning to change. The wars in Ukraine and the Middle East have highlighted how closely connected energy, geopolitics, and food security have become. Rising oil and gas prices do not just affect fuel bills or transport costs. They also feed into the global food system through fertilisers, farming inputs, and agricultural supply chains.

The result is that food inflation increasingly reflects more than temporary shortages or poor harvests. It is becoming part of a broader structural shift towards a world shaped by geopolitical fragmentation, supply chain resilience, and volatile inflation.

For thematic investors, this shift is important because food security is no longer simply an agricultural issue. It is increasingly becoming a strategic one.

Why fertiliser matters

One of the clearest examples of this transmission mechanism is nitrogen fertiliser, which is heavily dependent on natural gas, and accounts for a large proportion of farm production costs. When energy prices rise sharply, fertiliser prices usually follow. Farmers then face higher input costs for planting crops such as corn, soybeans, and wheat.

However, these effects are not immediate. Farmers often hedge purchases and buy fertiliser months in advance, meaning the impact can take time to work its way through the system. That lag effect is one reason food inflation can remain elevated even after energy prices begin to stabilise. When fertiliser prices rise sharply, farmers may delay purchases or reduce application rates, potentially lowering crop yields further down the line.

This dynamic is already attracting increasing attention from policymakers. The Bank of England recently warned that higher energy and fertiliser costs could push UK food price inflation higher through the remainder of 2026 and into 2027. Meanwhile, disruption to shipping routes through the Strait of Hormuz has already begun affecting supplies of fertiliser and agricultural inputs, adding further uncertainty across global food markets.

The wider point is that food inflation is rarely driven by one factor alone. Weather patterns, geopolitics, labour shortages, and trade tensions all interact within a long and highly complex supply chain.

Climate pressures also continue to build. Droughts, flooding and extreme heat are becoming more frequent in key agricultural regions. There is also a near-term risk of a Super El Niño, which threatens to add further volatility to crop yields and commodity prices. Taken together, these pressures suggest the global food system is entering a more fragile and unpredictable phase.

A changing investment backdrop

This environment fits within Sarasin’s use of broad market regimes to aid equity investing. We classify the current regime as Global fragmentation and believe it has been in place since 2021. Rather than assume the world returns to low-inflation and balanced equilibrium conditions that defined previous regimes in the 2000s and 2010s, today we recognise an environment of geopolitical tension, and less flexible supply chains. As such we believe there are higher chances of inflationary spikes occurring more often.

Food security sits naturally within this thinking. Countries are increasingly prioritising resilience, strategic supply and food security alongside efficiency. Governments are becoming more sensitive to strategic dependencies in energy, agriculture, and critical supply chains. Trade flows are evolving as geopolitical relationships change.

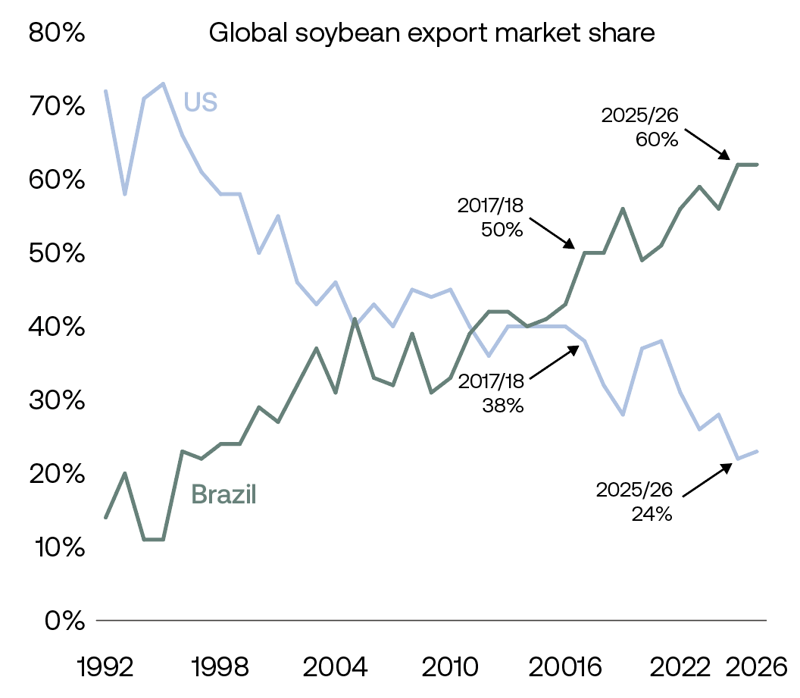

The rise of Brazil as a major agricultural exporter, for example, has altered global grain and soybean markets over the past two decades and given countries such as China greater flexibility in sourcing agricultural imports (see Figure 1).

At the same time, agricultural inflation shocks are occurring more frequently and often taking longer to unwind. This creates a more supportive backdrop for businesses linked to food security, agricultural productivity, and supply chain resilience.

Figure 1: Shifting agricultural power

Brazil has overtaken the US as the world’s largest soybean exporter, reflecting changing trade flows and growing geopolitical fragmentation.

Source: US Department of Agriculture, Sarasin & Partners, 1992-2026

Accessing the theme through fertilisers

One area of focus is fertiliser production. For example, within the Sarasin Food & Agriculture Opportunities strategy, CF Industries provides exposure to nitrogen fertilisers. The company is one of North America’s largest producers and benefits from access to relatively low-cost US natural gas.

That matters because fertiliser markets are highly sensitive to geopolitical disruptions and regional energy prices. Around half of global urea exports pass through the Middle East, including key shipping routes linked to the Strait of Hormuz.

When conflict or energy shortages disrupt supply, fertiliser prices can move sharply higher. Producers with lower-cost operations may therefore benefit from widening margins and stronger cash generation.

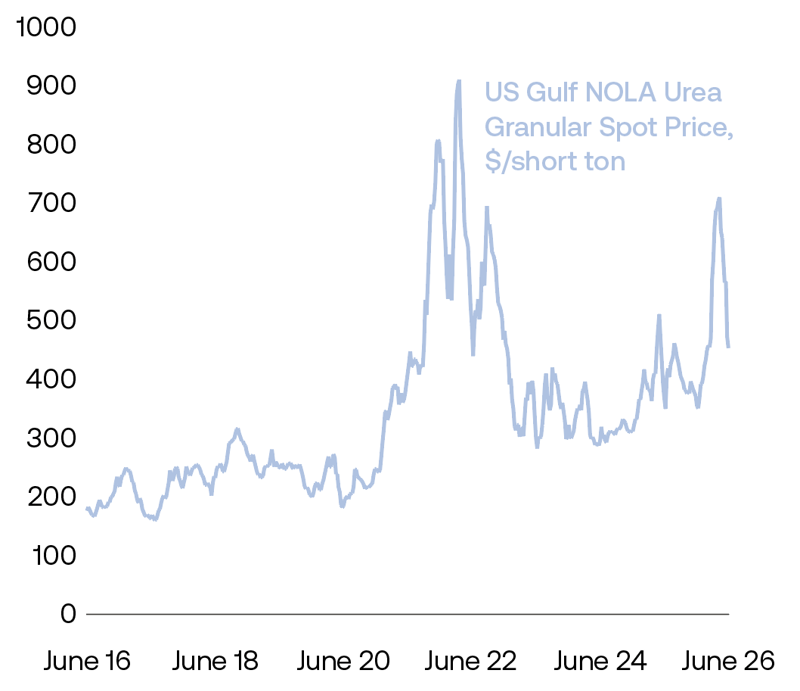

While fertiliser markets can be volatile, they also illustrate how food security and energy security are becoming increasingly interconnected (Figure 2).

Figure 2: A warning sign for food inflation

Rising fertiliser prices often feed through to higher food costs, although the impact can take months to appear.

Source: Bloomberg; Green Markets, Sarasin & Partners, 2016-2026

Improving productivity

A second area of focus is agricultural productivity. Rising input costs and climate pressures are increasing the need for farmers to produce more food using fewer resources. This is accelerating investment in precision agriculture, automation and data-driven farming technologies.

John Deere is one example of a business exposed to this trend. The company has expanded beyond traditional agricultural equipment into areas such as automation, digitalisation, and precision spraying technology. These tools can help farmers reduce fertiliser use, improve yields and manage costs more efficiently.

Over time, technologies that improve productivity and resilience are likely to become increasingly important as the agricultural sector adapts to tighter resource constraints and greater climate variability.

Food security as a long-term theme

The broader investment opportunity extends beyond any individual company. Sarasin’s Food & Agriculture Opportunities strategy focuses on several long-term themes shaping the global food system, including food security and resilience, rising productivity, and changing consumer diets and preferences.

These themes are supported by structural trends that are likely to persist for many years, including population growth, ageing, weight loss drugs, and climate pressures.

While short-term commodity prices will always fluctuate, the long-term challenge of producing sufficient, affordable, and sustainable food is becoming more significant. For investors, that means food security is increasingly moving from the margins of portfolio discussions towards the centre of them.

Within our Food & Agriculture Opportunities fund, we have reintroduced fertiliser producers CF Industries and Nutrien. We believe the market underappreciates the excess cash flow these businesses could generate as Middle East geopolitics tighten the global nitrogen market.

The fund already had significant holdings in grocery retailers such as Shoprite, Ahold, Costco, and Walmart, and contract caterers such as Compass and Aramark. Both business models can generally pass on inflation. Agricultural equipment manufacturers Deere, CNH, and AGCO are longer-term beneficiaries of rising adoption of precision farming technologies, particularly in Brazil, and are currently held as smaller positions.

In our broader global thematic, income, and multi-asset client products we own Compass, Costco, Ahold, and Deere as a subset of companies that benefit directly or indirectly from food inflation.

Key points

Rising energy and fertiliser costs are increasing pressure on the global food system and could keep food inflation elevated into 2027.

Food security is becoming a more important investment theme as geopolitics, climate pressures, and supply chain fragmentation reshape global agriculture.

Sarasin accesses this theme through areas including fertiliser production, agricultural productivity, and long-term food security and resilience.

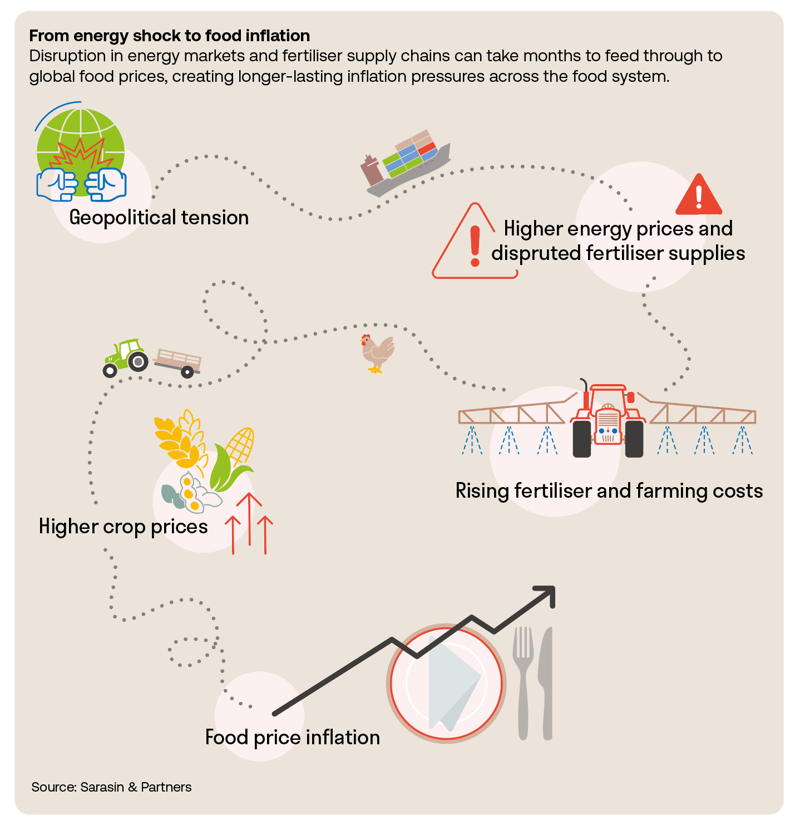

From energy shock to food inflation

Disruption in energy markets and fertiliser supply chains can take months to feed through to global food prices, creating longer-lasting inflation pressures across the food system.

Source: Sarasin & Partners, 2026

Important Information

This video is intended for retail investors and/or private clients. You should not act or rely on any information contained in this document without seeking advice from a professional adviser.

This is a marketing communication. Issued by Sarasin & Partners LLP, 50 George St, London, W1U 7DY. Registered in England and Wales, No. OC329859. Authorised and regulated by the Financial Conduct Authority (FRN: 475111). Website: www.sarasinandpartners.com. Tel: +44 (0)20 7038 7000. Telephone calls may be recorded or monitored in accordance with applicable laws.

This document has been produced for marketing and informational purposes only. It is not a solicitation or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice.

This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

Capital at risk. The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance. The index data referenced is the property of third-party providers and has been licensed for use by us. Our Third-Party Suppliers accept no liability in connection with its use. See our website for a full copy of the index disclaimers https://sarasinandpartners.com/important-information/.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2026 Sarasin & Partners LLP. All rights reserved. This document is subject to copyright and can only be reproduced or distributed with permission from Sarasin & Partners LLP. Any unauthorised use is strictly prohibited.