A simple guide to UK Individual Savings Accounts

An ISA (Individual Savings Account) is a tax-efficient way to save or invest money in the UK. ISAs allow you to earn interest, dividends and investment growth without paying UK income tax or capital gains tax on the returns.

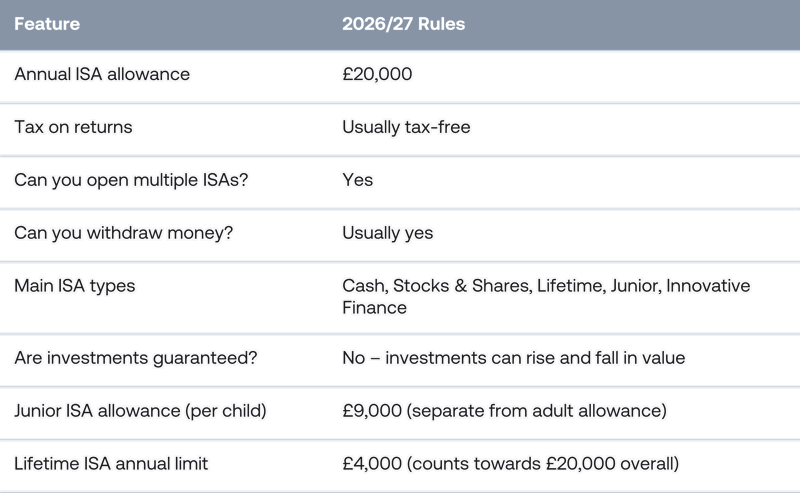

Introduced by the UK government in 1999, ISAs are designed to encourage long-term saving and investing. For the 2026/27 tax year, the annual ISA allowance remains £20,000, with the latest guidance published on the gov.uk website.

You can choose to hold cash savings, investments, or a combination of both within your ISA allowance.

ISA rules at a glance:

How does an ISA work?

ISAs act as a "tax wrapper" around your savings or investments. This means any interest, dividends or investment gains earned within the account are generally free from UK income tax and capital gains tax.

There are several different types of ISA available, each designed for different financial goals and attitudes to risk.

For example:

A Cash ISA may suit savers looking for stability and easy access to their money.

A Stocks & Shares ISA may suit long-term investors seeking higher potential returns, although investments can fall as well as rise in value.

The right ISA for you will depend on your financial objectives, time horizon and tolerance for risk.

What are the different types of ISA?

Cash ISA

A Cash ISA works similarly to a traditional savings account, but any interest earned is tax-free.

Cash ISAs may appeal to savers who:

Prefer lower risk

Want predictable returns

May need access to their savings in the short term

However, returns may be lower than inflation over the long term.

Important: Upcoming Cash ISA changes from April 2027

From 6 April 2027, the Cash ISA allowance for savers aged 65 and under will reduce from £20,000 to £12,000 per year. Savers aged 65 and over will retain the full £20,000 Cash ISA allowance. The overall annual ISA allowance will remain £20,000; any amount above the £12,000 Cash ISA limit can be placed in a Stocks & Shares ISA or other non-cash ISA. These limits apply to new contributions from 6 April 2027 only – existing Cash ISA balances are not affected. The 2026/27 tax year is the last full year under the current rules.

Stocks & Shares ISA

A Stocks & Shares ISA allows you to invest in assets such as:

Shares

Bonds

Investment funds

ETFs (exchange traded funds)

This type of ISA may offer greater long-term growth potential than cash savings, but investments can rise and fall in value and you may get back less than you originally invested.

Stocks & Shares ISAs are generally more suitable for long-term investing.

Lifetime ISA (LISA)

A Lifetime ISA helps eligible adults save for:

Buying a first home

Retirement

Key rules and limits:

You must be aged 18–39 to open a Lifetime ISA.

You can contribute up to £4,000 per tax year, and the government adds a 25% bonus (up to £1,000 per year).

Contributions can be made until the day before you turn 50.

The £4,000 annual LISA limit counts towards your overall £20,000 ISA allowance.

Properties purchased using a LISA must cost no more than £450,000.

Withdrawals for reasons other than a first home purchase or retirement (from age 60) incur a 25% government penalty charge, which effectively claws back the bonus and more.

Important: Lifetime ISA to be replaced in April 2028

The government has announced that the Lifetime ISA will be replaced by a new first-time buyer ISA in April 2028. The replacement product is expected to focus solely on helping people buy a first home, removing the retirement-saving option. The proposed new ISA aims to eliminate the 25% withdrawal penalty, with the government bonus likely paid as a lump sum at the time of house purchase rather than monthly.

Existing LISA holders will be able to continue contributing to their accounts after the new product launches. If you are eligible, opening a LISA now preserves your access to the current scheme and its benefits. The government has confirmed a consultation will take place in 2026 before final rules are set.

Junior ISA

A Junior ISA is a tax-efficient savings or investment account for children under 18.

Key rules:

The Junior ISA allowance for 2026/27 is £9,000 per child – this is entirely separate from the adult £20,000 ISA allowance and does not affect it.

A Junior ISA must be opened by a parent or legal guardian, but anyone (including grandparents, other relatives and friends) can contribute on the child’s behalf.

The money belongs to the child and cannot be accessed until they turn 18, at which point the account automatically converts to an adult ISA.

A child can hold one Cash Junior ISA and one Stocks & Shares Junior ISA at any one time.

Unused Junior ISA allowance cannot be carried forward to the next tax year.

Innovative Finance ISA

An Innovative Finance ISA allows investments in peer-to-peer lending platforms and other alternative finance products.

These ISAs can carry a higher level of risk and may not be suitable for all investors.

What is the ISA allowance for 2026/27?

For the 2026/27 tax year, the ISA allowance is £20,000.

This means you can save or invest up to £20,000 across your ISAs during the tax year without paying tax on eligible returns.

You can:

Put the full amount into one ISA

Split it across different ISA types

Contribute to multiple ISAs with different providers

The total amount contributed across all ISAs cannot exceed the annual allowance. Note that the Lifetime ISA has a separate sub-limit of £4,000 per year, which counts towards the £20,000 total.

Can you have more than one ISA?

Yes. Under current ISA rules, you can contribute to multiple ISAs in the same tax year, including more than one ISA of the same type.

For example, you could:

Hold several Cash ISAs

Invest in multiple Stocks & Shares ISAs

Split your allowance between savings and investments

As long as your total contributions remain within the annual ISA allowance, this is permitted.

What is a flexible ISA?

Some providers offer "flexible ISAs".

A flexible ISA allows you to withdraw money and replace it within the same tax year without affecting your annual ISA allowance.

For example:

You contribute £10,000 to a flexible ISA

You later withdraw £2,000

You can replace that £2,000 during the same tax year without reducing your remaining allowance

Not all ISAs are flexible, so it is important to check your provider’s terms and conditions.

Can you withdraw money from an ISA?

In most cases, you can withdraw money from an ISA whenever you choose.

However, withdrawing funds from a non-flexible ISA may affect how much you can pay back in during the same tax year.

Before making withdrawals, it is important to:

Check whether your ISA is flexible

Understand any penalties or restrictions

Review any loss of benefits or preferential rates

How do ISA transfers work?

If you are unhappy with your current provider or want to change your investment strategy, you can usually transfer your ISA to another provider without losing its tax-efficient status.

You may be able to transfer:

A Cash ISA to another Cash ISA

A Stocks & Shares ISA to another Stocks & Shares ISA

A Cash ISA into a Stocks & Shares ISA

A Stocks & Shares ISA into a Cash ISA (depending on the provider)

To preserve the tax benefits, always use the provider’s official ISA transfer process rather than withdrawing the money yourself.

Different providers may charge transfer or exit fees, so it is important to read the terms and conditions carefully before making changes.

Are ISAs worth it?

For many UK savers and investors, ISAs can be an effective way to build wealth tax-efficiently over time.

Potential benefits include:

Tax-free interest and investment growth

Flexibility across savings and investment options

Long-term compounding potential

Simpler tax reporting

The most suitable ISA will depend on your personal circumstances, financial goals and appetite for risk.

ISA Frequently Asked Questions

Do you pay tax on an ISA?

No. Interest, dividends and investment gains earned within an ISA are generally free from UK income tax and capital gains tax.

Can I open more than one ISA?

Yes. You can contribute to multiple ISAs in the same tax year, provided your total contributions stay within the annual ISA allowance.

Is a Cash ISA better than a Stocks & Shares ISA?

It depends on your financial goals and tolerance for risk. Cash ISAs may suit cautious savers seeking stability, while Stocks & Shares ISAs may suit long-term investors willing to accept market fluctuations in pursuit of potentially higher returns.

Can I transfer an ISA?

Yes. You can transfer ISAs between providers without losing the tax benefits, provided you use the official ISA transfer process.

What happens to my ISA at the end of the tax year?

Your ISA remains open and retains its tax-efficient status. However, any unused ISA allowance for that tax year is usually lost and cannot be carried forward.

What is the Junior ISA allowance?

The Junior ISA allowance for 2026/27 is £9,000 per child. This is separate from the adult ISA allowance and does not affect it.

Is the Lifetime ISA being scrapped?

The government has announced that the Lifetime ISA will be replaced by a new first-time buyer ISA in April 2028. Existing LISA holders will be able to continue contributing indefinitely. If you are eligible, opening a LISA now is still an option worth considering – seek independent financial advice if you are unsure.

This article is for informational purposes only and does not constitute financial or tax advice. ISA rules are set by the UK government and HMRC and are subject to change. For the most up-to-date information, visit Gov.UK. Tax treatment depends on individual circumstances.

Important Information

The information on this webpage has been produced for educational purposes. Retail investors should not act or rely on any information contained on this webpage without seeking advice from a professional adviser.

This is not intended as a solicitation, or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice. The information on this webpage should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information on this webpage when taking individual investment and/or strategic decisions.

Capital at risk. The value of your investments and any income derived from them can fall as well as rise and you may not get back the amount originally invested. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance.

Issued by Sarasin & Partners LLP, 50 George Street, London, W1U 7DY. Registered in England and Wales, No. OC329859. Authorised and regulated by the Financial Conduct Authority (FRN: 475111).

© 2026 Sarasin & Partners LLP. All rights reserved.