Sarasin & Partners, in partnership with a group of 39 global investors representing $3.75 trillion in assets, have this week written to the US SEC’s Chief Accountant and Director for the Division of Corporation Finance to ask them to look into whether listed energy companies are providing required accounting disclosures. The investors are concerned that inadequate disclosure is hampering their ability to interpret the companies’ financial statements, potentially putting investors at risk and impeding market efficiency.

This letter is important at a time when climate change has become politicised, leading to the potential obfuscation over the real economic consequences that shifting technology, government policies and consumer preferences is having on a range of markets. It is vital that we protect and reinforce the core job of accountants, auditors and regulators in delivering reliable financial reports that are vital for long-term growth.

Reliable accounting is mission critical for efficient markets. Where financial statements mislead, this doesn’t just harm investors who may deploy capital to the wrong activities; it has the potential to harm staff, suppliers, customers and the public – all of which depend on a healthy corporate sector. Where the numbers overstate capital strength or performance, for example, they will tend to attract excessive capital, reducing cash flows available for alternative ventures, impairing economic resilience and growth.

To underpin confidence in financial reporting, objectivity and transparency are key. In particular, investors and other stakeholders need to know the critical accounting assumptions upon which the reported numbers depend.

In 2018, Sarasin & Partners published a paper outlining concerns that oil and gas companies were failing to disclose critical forward-looking assumptions, such as long-term oil and gas prices used in impairment testing, in their financial reporting.

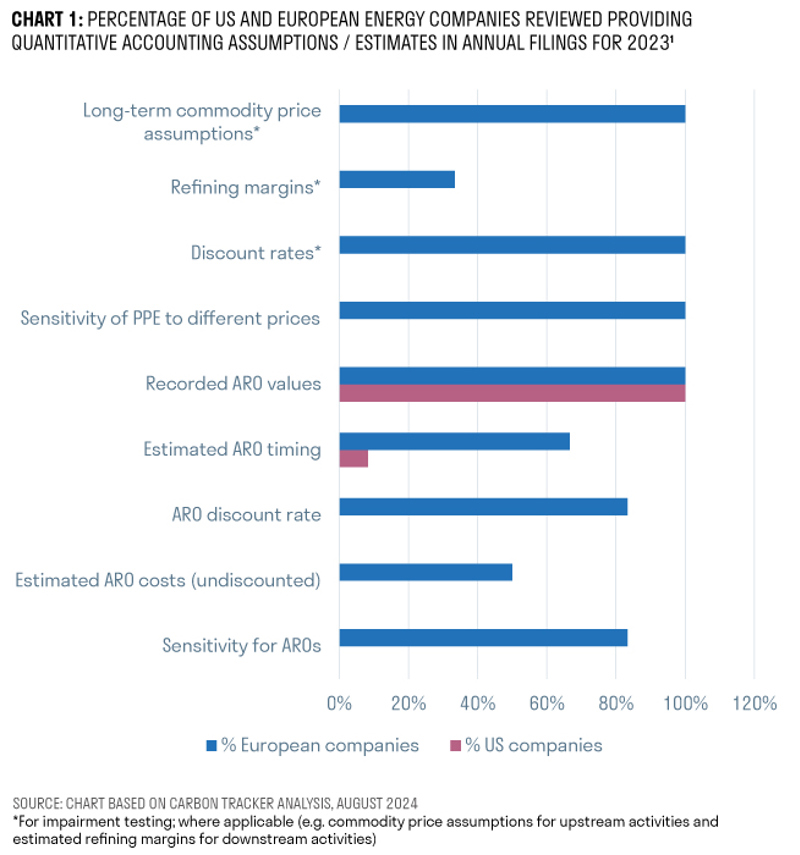

Six years on, we have seen a sea change in European oil and gas company disclosures. However, in the US, investors remain largely in the dark as to the critical forward-looking assumptions underpinning their balance sheets. Whether we consider long-term commodity prices, refining margins, discount rates, or associated sensitivities (see chart below).

Against this backdrop, Sarasin & Partners, in partnership with a group of 39 global investors representing $3.75 trillion in assets, has written to the SEC’s Chief Accountant and Head of Corporation Finance to ask them to look into whether this disclosure gap is consistent with the rules. Specifically, the investors ask how the apparent silence on key assumptions can be consistent with Regulation S-K, Item 303, which says that companies must disclose in their Management Discussion and Analysis (MD&A) the critical accounting estimates and assumptions that underpin their financial statements and are important to understanding the company’s financial position.

Under the Regulation, management is also required to disclose changes to these assumptions, as well as sensitivities to reasonable alternative assumptions, where this information is material[2]. This is particularly true at a time of rising uncertainty with accelerating decarbonisation and tightening climate policies.

The letter is copied to Financial Accounting Standards Board (FASB) and the federal audit regulator (PCAOB).

This letter is important at a time when climate change has become politicised, leading to the potential obfuscation over the real economic consequences that shifting technology, government policies and consumer preferences is having on a range of markets. It is vital that we protect and reinforce the core job of accountants, auditors and regulators in delivering reliable financial reports that are vital for long-term growth.

[1] Analysis by Carbon Tracker’s Accounting, Audit and Disclosure team based on a review of 2023 financial year annual filings. Companies covered in analysis include seven US energy companies (Occidental Petroleum, Exxon Mobil, Chevron, ConocoPhillips, Marathon Petroleum, Phillips 66, and Valero Energy), and six European energy companies (bp, Shell, Eni, Repsol, TotalEnergies, Equinor). Note on methodology: Disclosure of assumptions/estimates is scored 1; no disclosure 0 and partial disclosure 0.5. Scores removed from calculation where not applicable – e.g., refining margin estimates are only relevant when refining activities undertaken by the entity. In addition, this analysis focuses only on assumptions and estimates related to recorded AROs, not unrecorded AROs which arise where issuers assume, for instance, indeterminate lives for relevant assets. We have concerns over the transparency of such unrecognised AROs but do not consider this here.

[2] https://www.law.cornell.edu/cfr/text/17/229.303 - See paragraph (b)(3)

Important information

This document is intended for retail investors and/or private clients. You should not act or rely on this document but should contact your professional adviser.

This document has been issued by Sarasin & Partners LLP of Juxon House, 100 St Paul’s Churchyard, London, EC4M 8BU, a limited liability partnership registered in England and Wales with registered number OC329859, and which is authorised and regulated by the Financial Conduct Authority with firm reference number 475111.

This document has been prepared for marketing and information purposes only and is not a solicitation, or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice.

This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2024 Sarasin & Partners LLP – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin & Partners LLP. Please contact marketing@sarasin.co.uk.