Key points:

We have reviewed our thematic framework and introduced a new theme: Security.

Security is becoming a greater priority for governments, industries, companies, and individuals – and this trend will be increasingly impactful for financial markets over the coming years.

This theme has been building for a number of years – and has been accelerated by the dramatic reshaping of international relations under the second Trump Administration.

In keeping with our global thematic approach to investing, we have introduced a sixth major theme: Security. Here we explain why we have done this, and what it means for our portfolios.

Sarasin & Partners has long used our framework of structural, longterm trends, or themes, to guide our approach to investment. As I outlined in our Q4 2024 edition, we are committed to identifying and capitalising on the market opportunities offered by these enduring themes, to deliver value to our clients.

The core of our thematic philosophy is that markets, by focusing too much on the short term, underappreciate the long-term impact of broad, inexorable themes like shifting demographics, technological developments, and the growing challenge of climate change. The existence of these themes is no secret. However, institutional pressures to deliver short-term performance and behavioural biases that oversimplify complex issues often prevent investors from accurately assessing long-term impacts – causing them to overlook significant risks and opportunities.

At Sarasin, we believe a deeper understanding of these themes is integral to delivering the desired investment outcomes to our clients. To achieve this, our framework must remain dynamic and forward-looking, continually focusing on the themes we believe will be most significant to financial markets in the coming years and decades.

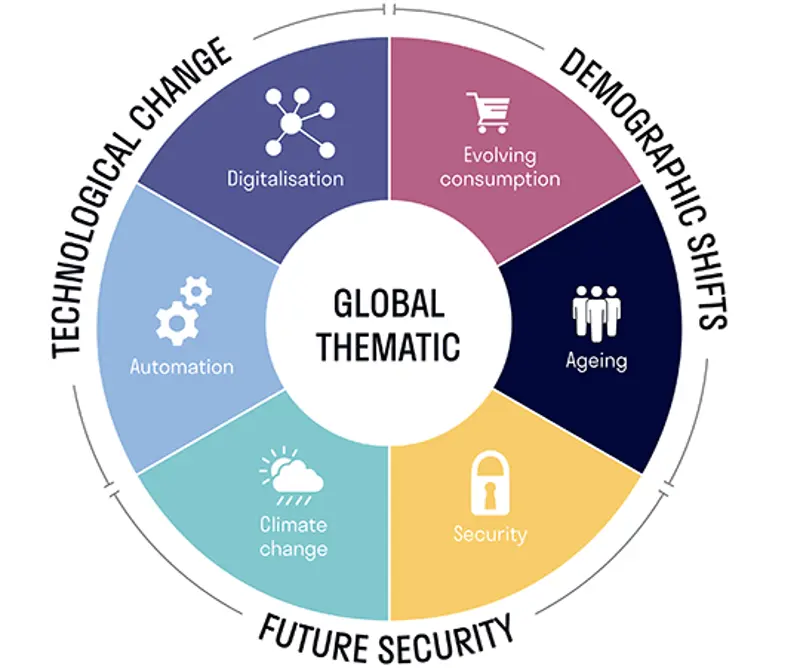

Following a recent review of this framework, we have decided to introduce a new theme to the mix, Security. This sits alongside our existing five themes – Ageing, Automation, Climate Change, Digitalisation, and Evolving Consumption – all of which remain as valid today as when they were first identified.

Why security?

We believe we are living through a profound shift in the geopolitical landscape. At its heart is the growing strain from increased global population, economic growth, and resource consumption, which exacerbates issues such as climate change, resource scarcity, and geopolitical instability – challenges too complex for any one nation to manage alone. These challenges have exposed the increasing weaknesses in the post-Cold War order. Yet with no consensus on the ideal political or economic system, nor a sufficiently shared global identity, there is currently no realistic pathway to a single unified solution.

These fundamental shifts have recently become more pronounced, as evidenced by the foreign policy direction taken by the new Trump administration in the US. As Subitha Subramaniam explored in our Q3 2024 edition, the relative stability of a unipolar, US-dominated world in recent decades has frayed, and is giving way to a ‘multipolar’ world. With the US redefining its relationships with both traditional allies and rivals, China and other “non-Western” countries too are seeking to reshape the international order in their favour, using protectionism, trade wars, and even the rising threats of military action to further their interests.

Increasingly, financial decisions made by organisations and individuals worldwide are driven by security concerns rather than purely economic or efficiency driven motivations. The definition of 'security' has expanded significantly, covering not only direct threats like cyber and military actions but also broader vulnerabilities in global food and energy supply chains. It now also encompasses rising unease about the reliability and sustainability of established global networks for trade, investment flows, information exchange, and the free movement of people.

From an investment perspective, we see the Security theme as impacting all aspects of financial markets, both across and within asset classes – and so we are ensuring our work in this area is considered when researching every current and future investment.

A timely addition to our framework

While the inherent tensions in the international order have been building for many years, the events of the early 2020s –including the pandemic, the Russian invasion of Ukraine, and the re-election of President Trump – suggest that the cracks in the system have widened beyond repair, and we have entered a new era – one in which security will play a major role.

The actions of the new Trump administration, most obviously the extraordinary levels of tariffs announced on 'Liberation Day', are the final nail in the coffin for the 'Pax Americana' – the era of relative peace and stability, underpinned by a US commitment to a rules-based world order. This has sharply accelerated the trend towards 'power politics' where international relations are dictated by power dynamics and national interests, rather than global institutions or frameworks based on common rules and values.

This environment comes with risks, but also opportunities. For example, companies like cybersecurity specialists Fortinet and Palo Alto Networks should benefit from increased spending on combating sophisticated cybercrime. Similarly, with businesses and governments prioritising supply chain resilience, this is creating opportunities for companies that provide reliable access to energy, food, and critical materials. This will benefit companies involved in natural resources, like Rio Tinto, and the food supply chain, like Deere.

While we see these geopolitical shifts as relevant for almost every large, listed company, some industries and businesses are naturally more resilient. This could be because they are more domestically oriented, serving a local rather than international client base. The nature of the business may also mean it has very simplified supply chains, or limited exposure to geopolitical disruptions, or could even benefit from a more sympathetic regulatory regime, as policymakers seek to protect and nurture homegrown champions. Financial services businesses, such as CME Group and J.P. Morgan Chase, remain relatively resilient in this regard. Another example is the South America-based retailer MercadoLibre, which we view as comparatively well insulated against supply chain disruptions, potentially allowing it to benefit more from this environment than its peers.

How we group our themes

It’s worth highlighting here how Security fits within our wider thematic framework. As illustrated below, you can see that our six themes are grouped into three pairs, reflecting their shared characteristics.

In brief, Technological Change covers the innovation driving enhanced economic productivity; Demographic Shifts addresses population dynamics, and evolving spending habits; while Future Security represents some of the big societal challenges facing us all. In practice, all six themes are interconnected; in the global economy, it is the complex and continuous interactions between technology, demographics, and governance that drives financial markets over the long term.

A framework for success

At Sarasin, we are firm believers that a focus on understanding the most important structural trends or themes is the best way to make sense of an ever-more complicated world. Our updated thematic framework gives us a solid foundation to explore these themes, and deliver strong returns for long-term investors.

By adding Security to our thematic framework, we acknowledge its growing importance in shaping financial markets and we equip ourselves to understand its effects thoroughly – both the challenges it creates and the investment opportunities it unlocks – as this structural change permeates the global economy.

Please do get in touch with us if you have any questions about Security, or anything to do with our thematic investment approach.

Important information

This document is intended for retail investors and/or private clients. You should not act or rely on this document but should contact your professional adviser.

This document has been issued by Sarasin & Partners LLP of Juxon House, 100 St Paul’s Churchyard, London, EC4M 8BU, a limited liability partnership registered in England and Wales with registered number OC329859, and which is authorised and regulated by the Financial Conduct Authority with firm reference number 475111.

This document has been prepared for marketing and information purposes only and is not a solicitation, or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice.

This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2025 Sarasin & Partners LLP – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin & Partners LLP. Please contact marketing@sarasin.co.uk.