Healthcare has historically been one of the most attractive sectors for long-term investors, combining structural demand with resilience through economic cycles. As a thematic investor, we at Sarasin assess the sector through the theme of Ageing in particular.

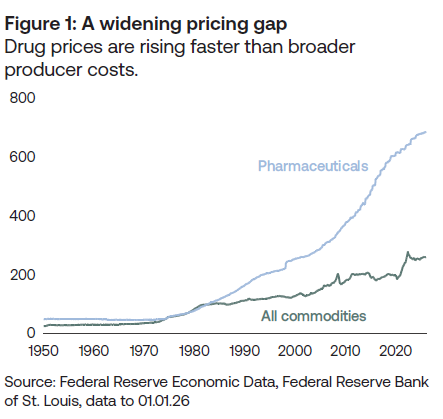

While healthcare spending rises globally, established models of pricing are being challenged. How, then, should investors assess the prospects for healthcare companies today? Historically, the sector followed a well-trodden path with a meaningful portion of pharmaceutical revenue growth, particularly in the US, coming from regular price increases within a system characterised by relatively limited direct pricing controls. However, in recent times that has been challenged and it is clear that growth model is now beginning to show signs of fatigue.

A positive for the sector is that healthcare spending already accounts for a significant share of developed world GDP – around 12–13% across OECD countries, according to the World Bank Group – and continues to rise faster than inflation. Despite this, governments and payers are increasingly focused on controlling costs. Meanwhile, pricing flexibility, once an implicit feature of the pharmaceutical model, is facing greater scrutiny.

Pricing power under pressure

Political attention on drug affordability has intensified in recent years. In the US, the Inflation Reduction Act introduced a new mechanism allowing Medicare to negotiate prices directly for selected high-cost medicines. While the immediate financial impact may be limited, the policy marks a symbolic shift. For decades, direct price negotiation was effectively off limits.

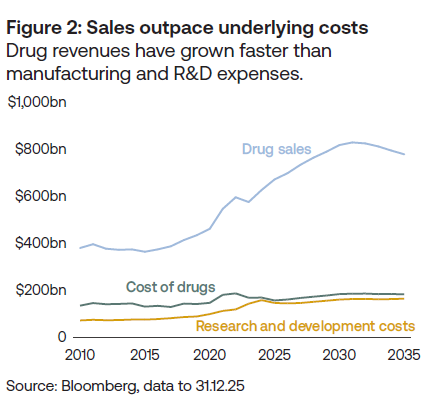

Looking across the profit and loss statements of major US and European pharmaceutical companies, rising drug prices have not generally been accompanied by comparable increases in manufacturing or research and development costs (figure 2).

Outside the US, pricing pressure has long been embedded in healthcare systems. European markets rely on national reimbursement frameworks and centralised negotiations. For example, in the UK the NHS decides which drugs it will pay for, how much it will pay, and under what conditions patients can receive them. In Asia, several markets use volume-based procurement programmes to drive down costs – as a government promises to buy large purchase volumes, so drug companies must offer steep price discounts.

Meanwhile, biosimilar competition continues to erode the economics of older branded drugs once patents expire, as it has always done. When the patents on these drugs expire, competing biosimilar versions enter the market, which lowers prices and reduces the profits of the original branded drugs.

Taken together, these forces do not eliminate pricing power entirely; innovative therapies that deliver meaningful clinical benefit can still command substantial launch prices but pharmaceutical growth is increasingly tied to patient penetration and access rather than sustained price escalation.

Volume as the dominant growth driver

The more interesting implication for investors is the growing importance of volume-driven business models.

Companies whose revenues depend primarily on utilisation – the number of procedures performed, tests run or patients treated – are structurally aligned with rising healthcare demand.

From a thematic perspective, demographics are the most obvious driver. Populations across developed markets are ageing rapidly, and older populations consume significantly more healthcare. Surgical interventions, diagnostic imaging, and chronic disease management all increase sharply with age.

Importantly, this demand is not cyclical. Chronic conditions require treatment regardless of economic conditions, and advances in medical technology are expanding the range of patients who can be treated effectively. In this environment, businesses tied to procedural volume rather than pricing discretion may offer more durable growth. We think certain medical technology companies, in particular, are well positioned. We highlight two examples below.

Intuitive Surgical: growth through procedures

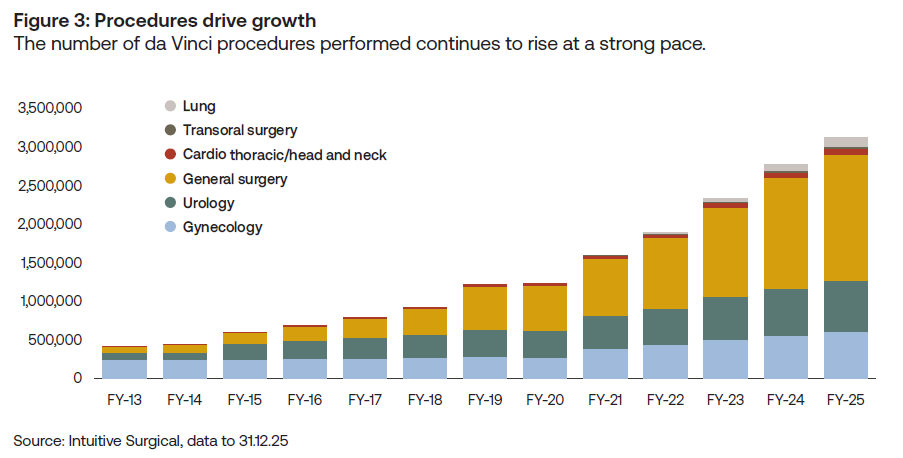

Intuitive Surgical is a US-based medical technology company that develops, manufactures, and markets robotic systems designed to improve clinical outcomes through minimally invasive surgery. It is perhaps the clearest example of a healthcare business built around procedural growth. Its da Vinci robotic systems enable surgeons to perform a range of gynaecological, bariatric, gastrointestinal, and other procedures through tiny incisions, while viewing patient anatomy in high-definition 3D from a dedicated console. Advances in surgical robotics are transforming major, invasive operations that once required lengthy hospital stays and months of recovery into routine outpatient procedures.

The company has also introduced an AI-enabled surgical “assistant” capable of monitoring procedures and providing real-time feedback to the surgeon. The model is simple and powerful. As the installed base of systems grows, so does the number of trained surgeons. As surgeon familiarity increases, the range of procedures performed expands. The addressable market remains large. Intuitive Surgical reported that approximately 3.2 million da Vinci procedures were performed in 2025, an increase of 18% from roughly 2.7 million in 2024.

With more than 300 million surgical procedures performed globally each year, we think that Intuitive Surgical is well positioned to meaningfully improve patient outcomes while also delivering significant economic benefits for hospitals. From a healthcare system perspective, robotic surgery can also improve efficiency. Shorter hospital stays and lower complication rates are attractive outcomes for systems operating under fiscal pressure. For investors, Intuitive Surgical represents a business whose economics are driven overwhelmingly by procedure volumes rather than pricing power.

Straumann: demographic dentistry

Switzerland-based Straumann, a global leader in dental implants and digital dentistry, offers a different example of the same underlying dynamic.

Dental implants have steadily become the preferred treatment for tooth loss, offering a more permanent and functional solution than traditional dentures. Yet global penetration remains relatively low. As awareness increases and dental technologies improve, implant procedures continue to expand.

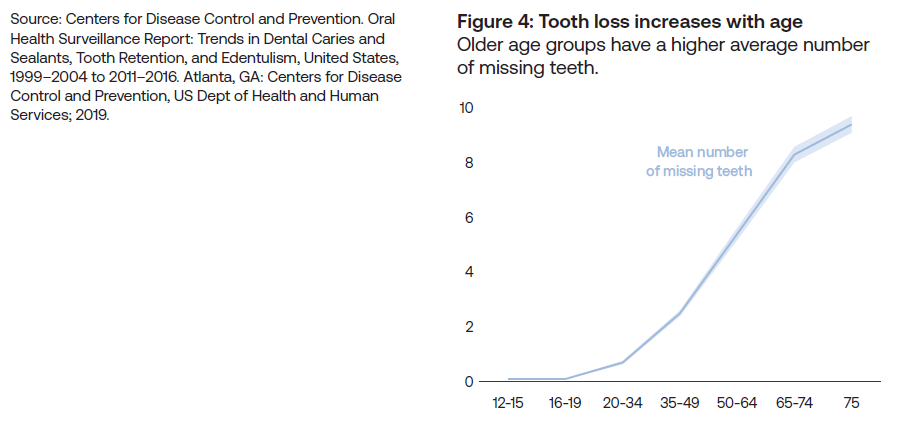

Demographics again play a central role. Tooth loss is strongly correlated with age (figure 4), and ageing populations naturally expand the addressable market for restorative dentistry. At the same time, rising incomes in emerging markets are also increasing access to advanced dental care.

Straumann’s strategy reflects this structural growth opportunity. The company operates across multiple price tiers and invests heavily in training dentists and integrating digital workflows into implant procedures. These investments help create a strong ecosystem around its products and encourage repeat usage. Like Intuitive Surgical, Straumann benefits from a model in which revenue growth is driven primarily by the number of procedures performed rather than by pricing increases.

Portfolio implications

Ageing remains a compelling, structural theme in global equities. The inexorable ageing of populations, alongside the rising prevalence of chronic disease, ensure that demand for healthcare services will continue to grow over time. However, the drivers of value creation within the sector are evolving. In an environment where pricing power is increasingly scrutinised, businesses linked to utilisation and procedural volume may offer more durable growth.

Companies such as Intuitive Surgical and Straumann illustrate this shift. Their revenues expand as more patients are treated and more procedures are performed – a model aligned with demographic reality and the needs of modern healthcare systems.

For long-term investors, the most attractive opportunities in healthcare may increasingly be found in businesses whose economics scale with utilisation rather than pricing alone.

Important information

This document is intended for retail investors and/or private clients. You should not act or rely on this document but should contact your professional adviser.

This document has been issued by Sarasin & Partners LLP of 50 George Street, London W1U 7DY, a limited liability partnership registered in England and Wales with registered number OC329859, and which is authorised and regulated by the Financial Conduct Authority with firm reference number 475111.

This document has been prepared for marketing and information purposes only and is not a solicitation, or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice.

This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2026 Sarasin & Partners LLP – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin & Partners LLP. Please contact [email protected].