Key points:

- The scope 1 to 3 emissions framework is essential for measurement, but says little about how businesses actually drive or reduce carbon emissions.

- Influential sectors with small footprints – such as exchanges, rating agencies, social media and audit – can enable huge amounts of high-carbon activity.

- Companies providing real solutions risk being misjudged if investors focus excessively on their scope 1 to 3 numbers.

Decarbonisation strategies must be rooted in market fundamentals not carbon footprinting. Emissions scopes are good for measurement but not for management. They tell us what a company’s carbon footprint is, but not how that business drives or reduces emissions in the real economy. For that we must start by understanding the essence of companies’ relationships with the carbon economy, and the pressure points for catalysing change.

Is the international system for carbon accounting consistently advancing efforts to tackle the climate crisis?

To sit in on an engagement discussion between investors committed to understanding climate risks and the companies they hold is, more often than not, an opportunity for a crash course in carbon accounting. Many hours are devoted to analysing companies’ scope 1 to 3 carbon emissions. The question is whether this is always time well spent.

There are good reasons to believe that, while scope emissions are vital for gauging the size of a company’s footprint, relying on them as the main yardstick for climate performance risks distracting investors from the real drivers of decarbonisation. The danger is that by focusing narrowly on these numbers, we miss the bigger question of how businesses actually influence the carbon economy – for better or worse.

A company with high emissions among its suppliers, for instance, may lack the levers to reduce them. Conversely, a business with a light footprint may be mission critical for high-carbon activities. If investors are to have meaningful conversations about decarbonisation, they must be grounded in business models and market realities, not just in scope-based accounting.

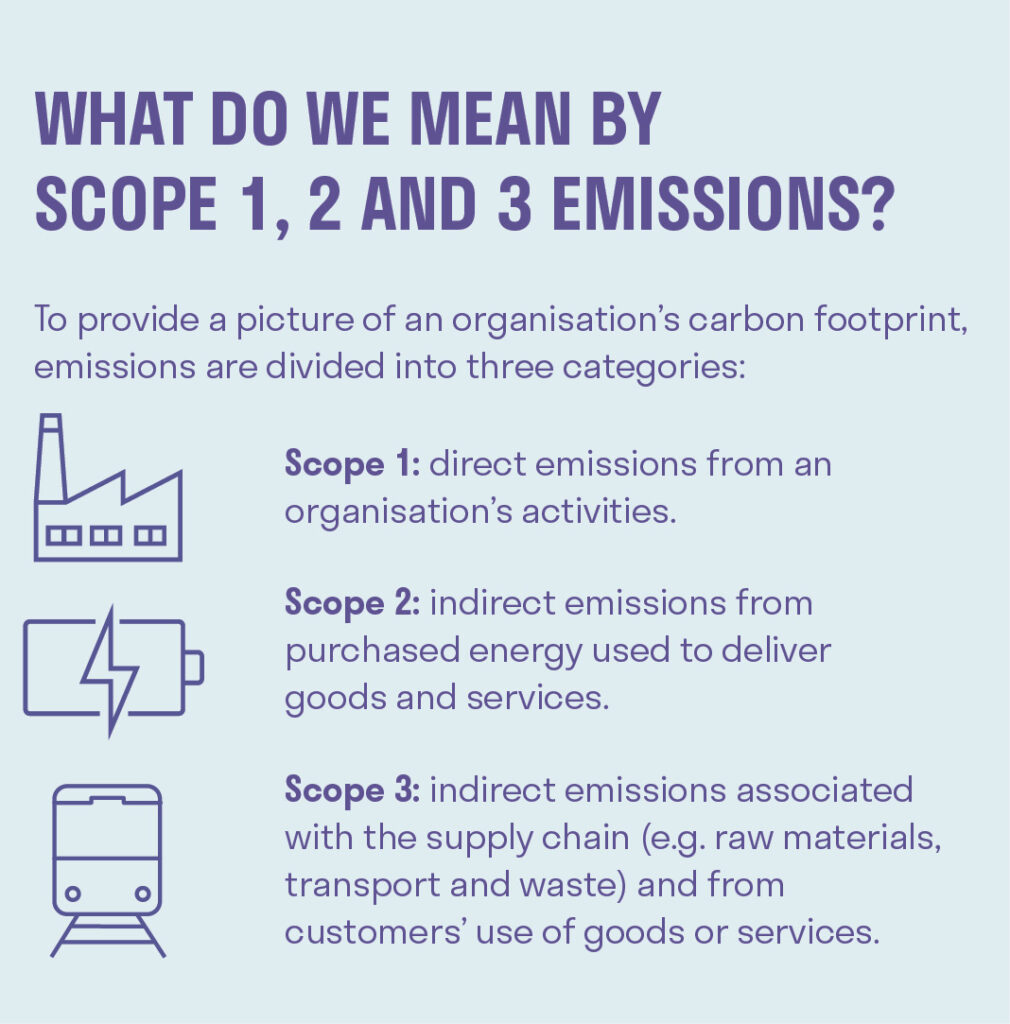

Over time, scope 1 to 3 emissions have become the dominant framework not just for measurement but also for judging climate performance. An industry of data providers and analysts has grown up around them. For example, the Science Based Target initiative (SBTi)[1] provides the main international benchmark for assessing whether a company’s targets are aligned with the Paris Agreement. It defines net zero as reducing scope 1, 2 and 3 emissions to zero – or to a residual level consistent with 1.5°C pathways – and then neutralising any remaining emissions at the target date and beyond.

The problem is that this lens can miss the very essence of how an entity contributes to or helps mitigate climate change. Consider companies with low direct and indirect emissions, but whose core activities enable high-emitting sectors to grow?

Hidden enablers of high emissions

Take financial exchanges. The direct carbon footprint is relatively small, including buildings, energy use and business travel. Even when growing energy use for data centres and supply-chain emissions are added, they remain lighter emitters than so-called ‘hard-to-abate’ sectors such as fossil fuel extraction, aviation, or steel production. Yet the scope framework stops short of asking what the exchange is actually financing. This, surely, is what matters most for real-world impact?

The think tank Carbon Tracker estimated in 2022 that global stock markets host companies holding three times more fossil fuel reserves than can be burned while staying within the Paris Agreement’s 1.5°C limit.[2]

Exchanges also channel capital to other carbon-intensive industries. The London Stock Exchange (LSE) calculates that these sectors make up almost 20% of global market capitalisation (excluding financials). Beyond equity, as of mid-2023, carbon-intensive entities had cumulative debt outstanding of US$5.5trn, equivalent to one-third of non-financial corporate debt, making it the largest category of outstanding non-financial debt.[3]

Yet in line with scope 1 to 3 orthodoxy, the exchanges say little about this matter. The LSE describes itself as a sustainability leader, but its climate disclosures do not mention the emissions it facilitates through equity and debt issuance for carbon-intensive businesses. Its decarbonisation targets focus on less meaningful operational emissions that “arise from the buildings and data centres we occupy and use, business travel, commuting, working from home and through the products and services we buy from our supply chain.”[4]

According to Carbon Tracker’s analysis, however, the LSE is one of the largest hubs for fossil fuel financing, hosting entities that are deploying capex into new reserve development consistent with a temperature pathway above 2.7°C.[5]

While, there are many aspects of the LSE’s decarbonisation efforts to applaud, a keener focus on what else could be done to catalyse a shift in financing away from harmful fossil fuels would not go amiss.

Credit rating agencies are another sector where we believe the scope 1 to 3 framework misses the mark. Moody’s, S&P and Fitch all report relatively low in-scope emissions and their decarbonisation plans focus on operational aspects like building energy use.[6] But their credit ratings unlock financing for high-carbon activities. Globally, carbon-intensive debt attracts higher credit ratings than other non-financial corporate debt, with 59% of issuance rated investment grade.[7]

This is despite carbon-intensive debt having longer maturities than average, exposing investors to greater decarbonisation risks. Some 46% of outstanding carbon-intensive debt extends beyond 10 years, and 16% exceeds 30 years, well past the 2050 net zero deadline under the Paris Agreement. For debt with a maturity of 15 years or more, 78% is investment grade.[8]

While rating agencies are coming under pressure from regulators to address this apparent blind-spot,[9] there is little sign that shareholders appear concerned. Having been widely criticised for mis-pricing risks in banks prior to the financial crisis, rating agencies can ill-afford to ignore the dangers of a climate-induced credit crunch.

Social media giants are also, we believe, neglected emissions enablers. While much attention has been (rightly) paid to the rising energy demand of artificial intelligence, which inflates their scope 2 and 3 emissions, few investors are challenging platforms like Meta for amplifying climate misinformation. But such ‘fake news’ undermines public trust in science, fuels resistance to climate policy and erodes political will – impacts invisible to scope accounting.[10]

Once we broaden our perspective to look for enablers of high-carbon activities, it’s not hard to find other examples. Auditors that ignore climate risks facilitate executives leaving potentially material physical or decarbonisation impacts out of financial reporting, relegating them to the non-financial bucket.[11] Lawyers, consultants, and marketing agencies all have small scope 1 to 3 footprints, but their influence on capital flows, disclosure, strategy, and public perception is substantial.

Solutions can also be masked by the carbon ledger

A simplistic focus on scope 1 to 3 emissions without regard to the broader influence of a business can also penalise companies providing solutions.

Take Deere, the agricultural equipment company best known for John Deere tractors. On paper, its emissions are high because it manufactures heavy machinery. But Deere is transforming itself into a precision agriculture company, embedding technology that allows farmers to cut fertiliser use, target irrigation, and enhance soil carbon sequestration. With agriculture accounting for 10 to 12% of global emissions,[12] companies that help to decarbonise food production – even if carbon benefits sit outside the scope 1 to 3 emissions envelope – need to be supported not upbraided.

None of this is to suggest that measuring scope 1 to 3 emissions is wrong. We need the data to track progress against the global carbon budget. Cutting direct and indirect emissions must also continue to be a priority for all companies. But carbon accounting does not tell us where the most powerful levers to drive decarbonisation reside. Investors’ time would be best spent acting on those pressure points that drive the greatest real-world decarbonisation; even if this means looking ‘out of scope’. This, in the end, will deliver the greatest long-term value for underlying clients.

[1] Corporate Net Zero Standard (V1.2 2024): https://sciencebasedtargets.org/net-zero

[2] https://carbontracker.org/reports/unburnable-carbon-ten-years-on/

[3] Meng, A, N. Sharma, N Ramkumar, and J. Kooroshy, “Tracing carbon-intensive debt: Identifying and calibrating climate risks in corporate fixed income”, LSEG, March 2024.

[4]LSEG Annual Sustainability Report 2024, p.25

[5] https://carbontracker.org/reports/unburnable-carbon-ten-years-on/

[6] See, for instance, Moody’s decarbonisation plan: https://www. moodys.com/sites/products/ProductAttachments/Sustainability/ moodys_decarbonization_plan.pdf; S&P’s TCFD report: https://www. spglobal.com/content/dam/spglobal/corporate/en/documents/ organization/who-we-are/sp-global-tcfd-report-2025.pdf

[7] Meng et al (March 2024)

[8] Meng et al (March 2024)

[9] The European Securities and Markets Authority, for instance, is due to issue final recommendations to tackle this: https://www.esma. europa.eu/sites/default/files/2024-12/ESMA84-2037069784-2196_ Final_Report_Amendment_to_Delegated_Regulation_447-2012_ and_Annex_I_of_CRA_Regulation.pdf

[10] https://www.lse.ac.uk/granthaminstitute/explainers/what-are-climate-misinformation-and-disinformation/

[11] Sarasin has spearheaded a number of investor initiatives over the past 10 years seeking to promote climate-aware accounting and audit to ensure financial statements continue to provide a true and fair view of capital, even in the face of rising transition and physical risks. See for instance: https://www.reuters.com/article/ world/exclusive-big-four-auditors-face-investor-calls-for-tougher-climate-scrutiny-idUSKBN1Y21XH/

[12] https://www.sciencedirect.com/science/article/abs/pii/ S0959652624024223

Important information

This document is intended for retail investors and/or private clients. You should not act or rely on this document but should contact your professional adviser.

This document has been issued by Sarasin & Partners LLP of Juxon House, 100 St Paul’s Churchyard, London, EC4M 8BU, a limited liability partnership registered in England and Wales with registered number OC329859, and which is authorised and regulated by the Financial Conduct Authority with firm reference number 475111.

This document has been prepared for marketing and information purposes only and is not a solicitation, or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice.

This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2025 Sarasin & Partners LLP – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin & Partners LLP. Please contact [email protected].