While seasoned investors know that volatility is the reality they accept in their pursuit for attractive long-term returns, every market downturn manages to surprise and brutalise participants. Over the short to medium-term, emotions and sentiment drive markets as much as investment fundamentals. Fear stalks the nervous investor, suggesting that the latest ‘new paradigm’ means a recovery is unlikely and a totally different approach for future success is required.

We would suggest that while history doesn’t repeat, it does rhyme. While the reasons for each boom and bust are invariably different, (they need to be to surprise the majority of investors) the market’s tendency to over-react, during both the rise and the fall, remains a constant. However, we invariably find a way to muddle through and when one is least expecting it, the bear market has suddenly turned into a bull market, as greed replaces fear.

This article places current market events in the context of history and considers where we go from here. What do this year’s events mean for charity portfolios and what does the correction in asset values, compounded by high inflation, mean for sustainable spending plans?

Over the past 12 months, in real terms, UK government bonds have produced a return of -31%, index-linked bonds have not offered inflation-proofing and have fallen by -33%, and global equities declined by 10%.

While there will be winners and losers, we expect the average charity portfolio will have lost about 20% of their value in real terms.

So, what does this look like in the context of previous periods of bad investment returns?

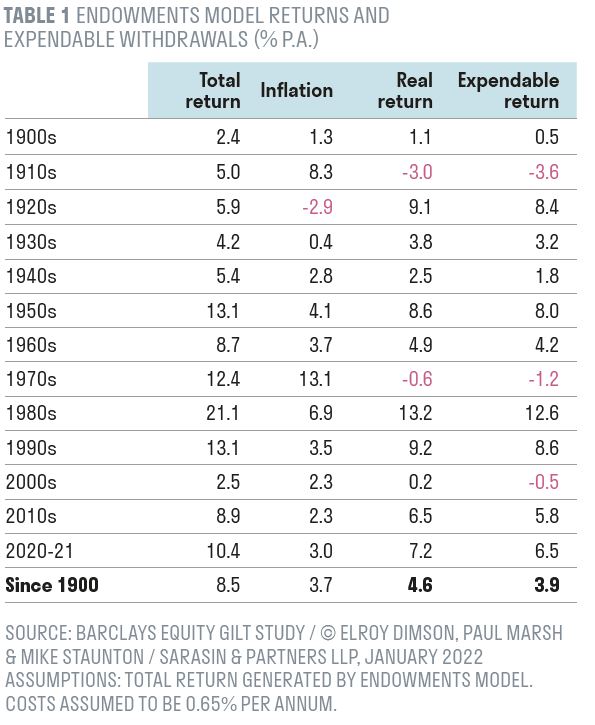

In Table 1, we review the returns produced by the Endowments Model in each decade since inception from an absolute, real and expendable (after costs) basis. This table was produced in our latest edition of the Sarasin Compendium of Investment with data to the end of 2021.

There have been three dreadful decades when spending any element of the return would have resulted in a reduction in the real value of the assets: the 1910s, the 1970s and 2000s. In each instance, the ‘damage’ was done in just a couple of years.

In the 1900s, 1930s, 1940s, and 1960s, there was a sustainable expendable return, averaging about 2.4% per annum. Interestingly, this was typically lower than the income that would have been generated by the natural asset allocation of the portfolio. Maintaining the real value of the portfolio during these specific decades would have required one to reinvest a reasonable proportion of the income generated each year. A reversal of how people think about total return investing today!

In the 1920s, 1950s, 1980s, 1990s and 2010s, there were significantly above average expendable returns of about 8.7% per annum.

What this exercise draws out is a pattern of distinct feasts and famines around the long-term sustainable expendable return of about 4% over the period as a whole.

What this draws out is that to spend in a consistent manner, it has always been important to underspend in the periods of strong returns, so that ‘real’ savings were built up to support consistent spending during fallow years.

But what about today?

As noted, over the first nine months of 2022, our Endowments Model suggests an absolute fall of about 10% compounded by inflation of 9%, resulting in a real fall of about 19%. To put this in context, there have only been five years since 1900 when we suspect real returns were worse: 1974, 1920, 1973, 1915 and 2008, where the damage was between -22% and -49%. Of course, the 1970s are infamous because the compound impact of ’73 and ’74 was a staggering -61%. While the rebound in 1975 of +68% was the single best year for our Endowments Model, the experience of the 1970s still traumatises those who experienced it and influences investment thinking today.

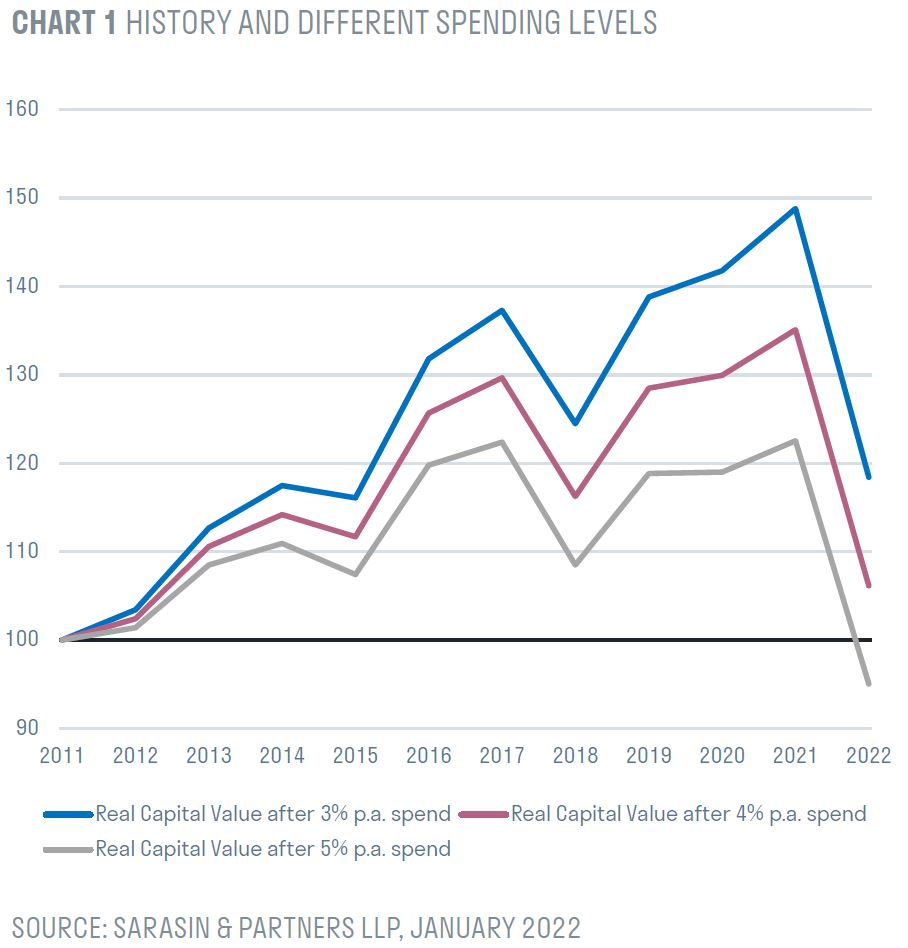

However, as noted, 2022 was preceded by over a decade of strong returns. Our work suggests that over this period, charities will have generated real returns of over 7% per annum. Unless trustees were spending 7% per annum, a significant real capital ‘buffer’ should have built up before the loss of value this year.

The first nine months of 2022 will have wiped out much of this: Chart 1 suggests buffers of 10% to 30% for those spending 3% to 4%, but those spending 5% will have seen their real capital gain wiped out.

The question of course is where from here?

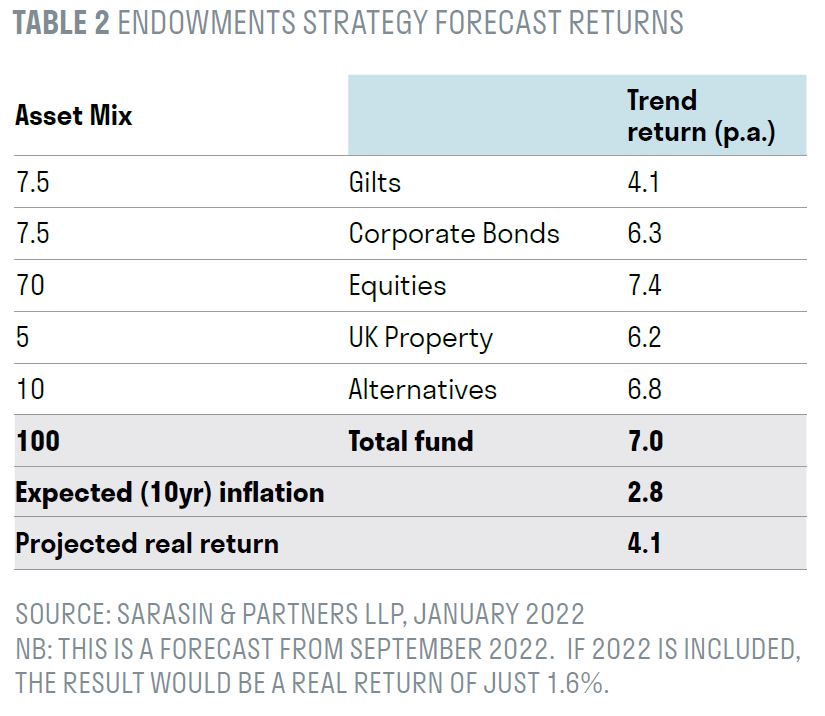

While it is difficult to forecast short-term market returns, our analysis suggests that longer-term trends can be more dependable. Bond yields are now materially higher than we have experienced in recent years, boosting projected returns from fixed income assets. The returns from equities will benefit from structurally higher inflation, a more attractive starting yield and lower valuations than were the case 12-18 months ago. While both bonds and equities might fall further in the short-term, catching the absolute bottom will always be very hard.

Table 2 outlines our projections for mainstream asset classes over the next 7-10 years:

The assumptions that underpin our projections for the various asset classes are detailed in the Sarasin Compendium of Investment.

Pulling the past and future together

We have cautioned for some time that the 2020s were likely to be a decade of weaker returns after markets were driven up over the previous 10-15 years by low inflation and falling bond yields, which pushed bond prices upwards and equity valuations higher, all against a backdrop of steady economic growth. A decade of feasting had to unravel at some point.

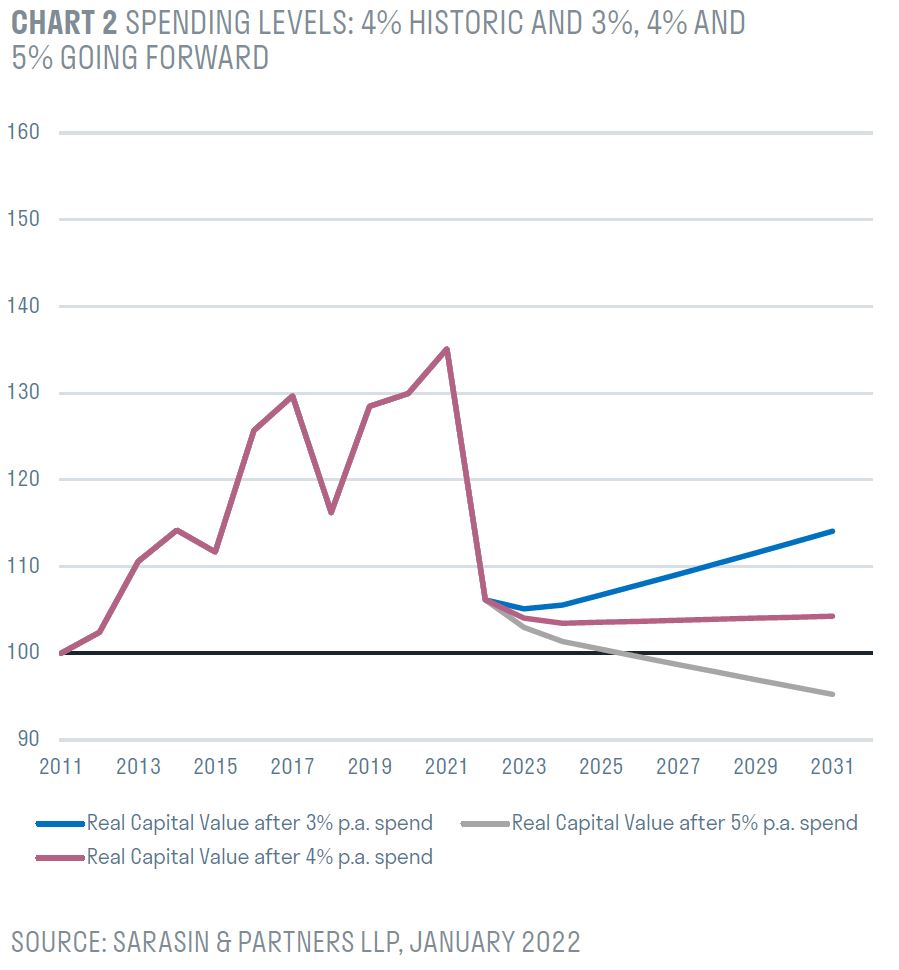

One never knows quite what the trigger will be for a correction and few could have predicted that this time it would be a combination of COVID and a war in Ukraine. Interestingly, if you look at the whole 20 years together, the real return – and thus, sustainable spending rate – is likely to be about 4% per annum, which is remarkably close to the very long-run averages.

While one could view this as a decade of feasting followed by a whole decade of famine, the actual shape of a weak decade is more likely to be an ugly 12-18 months of capital destruction (which we are quite possibly reaching the end of), followed by a period of attractive returns thereafter. At which point, markets will probably have become over-valued once again in time for the next correction!

So, to return to the core question; how much can a charity afford to spend over the next 7-10 years?

It will first depend on their historic returns and how much they withdrew over the past decade. However, as Chart 2 shows, if one had achieved average returns and spent the long-term sustainable average of 4% over the past decade, even after the torrid past 12 months, one should be able to continue to spend 4% per annum over the next decade. Across the whole 20-year period, one ends with a little more capital in real terms than when one started.

However, a word of caution. On the one hand, a consistent 4% spending rate over the entire 20-year period would ensure maximum benefit to current beneficiaries, while maintaining the real capital value for the future – so, balance achieved. On the other, it doesn’t leave much of buffer for the next storm, which will surely bedevil markets at some point in the future.

As a consequence, while some charities will seek to continue to maximise their spending at the 4% level, we suspect many trustees will choose to be prudent in the immediate future and set their spending levels to nearer 3% than 4%, only increasing spending when their capital buffers have been rebuilt to more comfortable levels and profits have been achieved, as opposed to merely forecast!

Important Information

This document has been issued by Sarasin & Partners LLP which is a limited liability partnership registered in England and Wales with registered number OC329859 and is authorised and regulated by the UK Financial Conduct Authority. It has been prepared solely for information purposes and is not a solicitation, or an offer to buy or sell any security. The information on which the document is based has been obtained from sources that we believe to be reliable, and in good faith, but we have not independently verified such information and we make no representation or warranty, express or implied, as to their accuracy. All expressions of opinion are subject to change without notice.

Please note that the prices of shares and the income from them can fall as well as rise and you may not get back the amount originally invested. This can be as a result of market movements and also of variations in the exchange rates between currencies. Past performance is not a guide to future returns and may not be repeated.

Neither Sarasin & Partners LLP nor any other member of the Bank J. Safra Sarasin group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of his or her own judgment. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document. If you are a private investor you should not rely on this document but should contact your professional adviser.

© 2022 Sarasin & Partners LLP – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin & Partners LLP.