“Alice laughed: "There's no use trying," she said; "one can't believe impossible things." "I daresay you haven't had much practice," said the Queen. "When I was younger, I always did it for half an hour a day. Why, sometimes I've believed as many as six impossible things before breakfast.”

– Alice's Adventures in Wonderland, Lewis Carroll

As an increasing number of the population is vaccinated, a rolling global recovery is unfolding, creating a wonderland of sorts for equity investors. Corporate profits are recovering at an impressive rate: the Q1 earnings season was 21% stronger than forecast1 and US corporate earnings have already exceeded pre-COVID levels. Business leaders are optimistic about the future. The future cashflows of the largest global companies are now assumed by investors to be worth 24% more than immediately before the pandemic struck2. How is this possible and for how much longer will it last? And how should equity investors position their portfolios?

Curiouser and curiouser

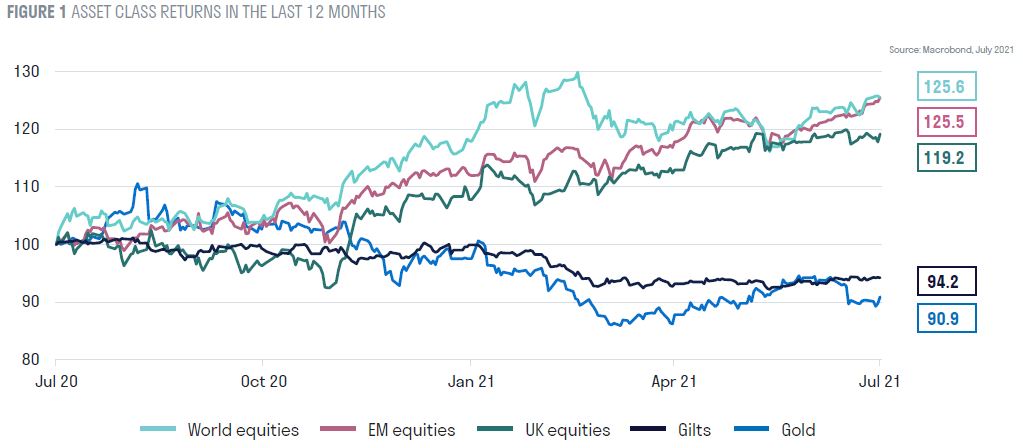

The sheer speed of the recovery has created a bull whip effect in the global economy. The rapid collapse in demand, the inability to operate factories with social distancing, and the run-down of inventories in 2020 created shortages for essential inputs. The 2021 G7 leaders’ communique claimed $12 trillion of fiscal support has already been provided during the pandemic and the size of the coordinated central bank balance sheet expansion dwarfs the quantitative easing seen following the Global Financial Crisis. Economic expansion is highly likely to remain above trend into 2022, although there are some indications that shortages and price increases are acting as a constraint on growth in some areas, such as housebuilding or auto production. This equity wonderland has rewarded investors, with all MSCI All Country World Index industry groups producing positive returns year to date3. Cyclical industries with lower valuations and strongest earnings upgrades such as energy, financials and materials, have led the market. Laggards have been the more defensive sectors such as utilities, staples and healthcare that lack relative earnings momentum and where valuations are undermined by higher discount rates.

So far, so wondrous, but the post-pandemic economic and market environment is not normal. The COVID -19 pandemic should be viewed as a natural disaster, and as a result, is more comparable to the post-WW2 era than the GFC. When looking towards the future, equity investors should beware orthodox economic analysis and a reliance on recent stock market history. Enormous fiscal and monetary stimulus have been put in place to avoid a post GFC-type malaise. The resulting recovery has exceeded all expectations and the effect on supply chains has led to surging prices.

How much longer can it last?

The long-term outlook for inflation is the single most important question facing investors because it will drive policy and asset pricing. The US 10-year government bond yield’s move to below 1.5% has been explained by bearish positioning and a belief in the Federal Reserve’s resolve, supported by aggressive central bank purchases.

However, the Federal Reserve meeting on 15-16 June removed the market’s assumption that the outlook for policy support would remain unchanged through the summer months, regardless of the economic data. Although the policy adjustment was subtle and interest increases not the central case until 2023, the meeting revealed disagreements and raised uncertainty. It appears that the Fed is less committed to average interest rate targeting and will be less tolerant of rising inflation expectations and a super-hot economy.

There is broad acceptance that inflation is approaching a peak. This does not mean that inflation cannot exceed expectations. The US consumer price index has risen at an annualised rate of 5.8% over the last six months4. Much of this is indeed transitory and can be explained by a spike in used car prices. However, economic activity is buoyant, inflation expectations are rising, there is further reopening pressure to come, and many companies report challenges attracting staff. Consumer balance sheets are unusually strong, disposable income is high and there is unfulfilled pent-up demand. It seems likely that the surge in inflation is likely to prove less transitory than generally assumed, as demand exceeds supply, leading to continued upward surprise. This will sap investor confidence over time, even if the data that proves this is not delivered until after the summer months.

Furthermore, the world is on the cusp of great change. Sustainability is a welcome and necessary priority, but improving environmental and social outcomes are inflationary. The labour force is close to shrinking in developed economies as populations age and the birth rate declines. The addition of 700 million workers to the global labour force from China and the former Soviet Union will not be repeated. The deflationary pressure on consumer prices from technology may well be less impactful in the future now prices are so transparent. 1970s style inflation is most unlikely, but the era of pervasive disinflation is behind us.

Are we approaching a peak for earnings?

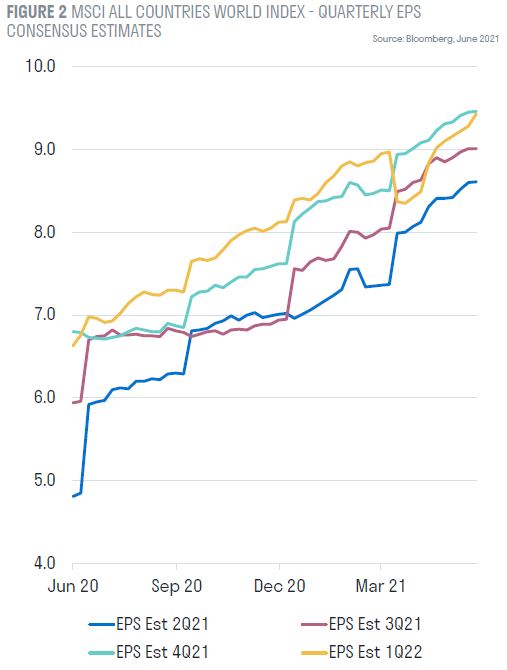

US earnings have beaten forecasts by around 20% for each of the last four quarters5. The breadth of US earnings revisions is the highest it has been for 20 years. Although a strong economy will continue to take profits higher, the extent to which analysts’ published forecasts continue to be surpassed will wane as margins are constrained by rising costs.

Credit Suisse estimates that 65% of a typical global non-financial corporate’s costs are labour. The rest is made up of raw materials (10%), with the balance in interest (3%), tax (5%) and depreciation (17%). It is hard to find raw materials that are not rising in price today. Oil bottomed at $35 in October 2020, has subsequently doubled and may well rise further as supply capital expenditure was cut. Companies are experiencing shortages in critical components such as semi-conductors. Global corporate tax rates will see upward pressure, supported by global coordination. Interest rates and credit spreads are at such low levels that borrowing costs can hardly fall further.

However, whether companies suffer a more prolonged margin squeeze will ultimately be determined by the extent to which they are forced to offer higher wages. Although the global economy has spare capacity today, there are skills shortages, and wage growth is exceeding expectations, as firms report challenges attracting staff.

As economic momentum peaks, companies will benefit less from recovering revenues and cost cutting. Consequently, net income margins for many companies will come under pressure in the next 24 months. According to Morgan Stanley, consensus US net income margins for 2022 are 100bp above all time previous highs. The extent of this squeeze on margins is not embedded in market expectations.

So how should equity investors react?

The consensus had been that bullish conditions would last through the summer, but with the business cycle unfolding so rapidly, this is likely to be complacent. Equity markets should now be discounting conditions we might experience in the first half of 2022. Can we assume that for the coming twelve months this wonderland – strong growth, abundant liquidity support, gentle inflation, low interest rates and elevated equity multiples – persists?

What does this mean for portfolio construction?

Greater volatility is likely, but when? To avoid being tripped up, we think investors should follow four guidelines when it comes to positioning:

- Diversify portfolios evenly across our themes, corporate characteristics and industry groups.

- Minimise factor or style risk.

- Maintain valuation discipline with an emphasis on attractive relative valuations in a world where nothing is cheap. Growth stocks should no longer be bought at any price.

- Ensure portfolio holdings have high specific (idiosyncratic) return potential.

Long term, the investment landscape will be dominated by the post-COVID thematic winners and disruptors that our process is designed to select. Emboldened government policies aligned to a greener, safer and more equitable world will determine the companies that prosper.